Variation in price elasticity as price of output

The only supply curve which has price elasticity which varies as the price of output increases is within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Hello guys I want your advice. Please recommend some views for above Economics problems.

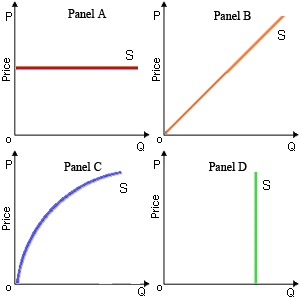

The only supply curve which has price elasticity which varies as the price of output increases is within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

Hello guys I want your advice. Please recommend some views for above Economics problems.

Can someone please help me in finding out the accurate answer from the following question. With similar market demand for its product and similar market labor supply curve, employment will be maximum when the firm is: (1) Pure comp

Normal 0 false false

The absolute intensity of one consumer’s preferences and tastes as compared to the absolute intensity of the other consumer’s tastes and preferences is as: (1) Dependent on the supplies of specific products. (2) Individually recognized in

Explain the term PHP?

The slopes of demand and supply curves are frequently: (w) misleading as guides to price elasticities. (x) independent of the units measuring changes in price and quantity. (y) highly dependent upon each other. (z) used to forecast changing consumer t

Select the right ans wer of the question. The Reciprocal Trade Agreements Act: 1) exempted American exporters from the Sherman Antitrust Act. 2) provided technological assistance to developing countries. 3) brought about considerable reductions in American trade barri

The slope of the ray by the origin which is tangent to point b equivalents to: (w) the reciprocal of the price elasticity of demand. (x) P / Q. (y) 0a / 0c. (z) the price elasticity of supply. Q : Jeremy Bentham utilitarianism Possible Possible utilization of a ‘felicific calculation’ to recognize punishments for the crimes was derived from: (1) Medieval scholasticism. (2) Say’s Law. (3) Gresham’s Law. (4) Marshall’s Maxim. (5) Jeremy Bentham&r

Possible utilization of a ‘felicific calculation’ to recognize punishments for the crimes was derived from: (1) Medieval scholasticism. (2) Say’s Law. (3) Gresham’s Law. (4) Marshall’s Maxim. (5) Jeremy Bentham&r

When raising subscription rates to the News and Observer from $8 to $10 monthly cause newspaper sales to drop by 180,000 to 120,000 copies daily, using the arc elasticity formula, then price elasticity of demand equals to: (1) 0.9. (2

The law of supply defines that there is a positive relationship among: (1) The Price and quantity supplied. (2) Technology and production. (3) Purchases and the accessibility of goods. (4) Supply and the demand it makes. Discover Q & A Leading Solution Library Avail More Than 1418934 Solved problems, classrooms assignments, textbook's solutions, for quick Downloads No hassle, Instant Access Start Discovering 18,76,764 1952203 Asked 3,689 Active Tutors 1418934 Questions Answered Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!! Submit Assignment

18,76,764

1952203 Asked

3,689

Active Tutors

1418934

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!