Perfectly inelastic supply of labor

Glynn’s supply of labor is perfectly inelastic at: (1) point a. (2) point b. (3) point c. (4) point d. (5) point e. Can anybody suggest me the proper explanation for given problem regarding Economics generally?

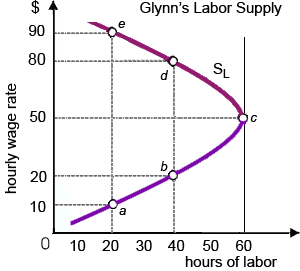

Glynn’s supply of labor is perfectly inelastic at: (1) point a. (2) point b. (3) point c. (4) point d. (5) point e.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?

At the price P1, this purely competitive Christmas tree industry is within: (w) long-run equilibrium. (x) short-run equilibrium. (y) market period disequilibrium. (z) short-run disequilibrium. Q : Define feature of perfectly inelastic A perfectly inelastic demand curve: (w) is an imaginary mathematical construct, and does not exist within reality. (x) corresponds to a perfectly horizontal line. (y) represents a good which absorbs only a small portion of consumers’ budgets. (z

A perfectly inelastic demand curve: (w) is an imaginary mathematical construct, and does not exist within reality. (x) corresponds to a perfectly horizontal line. (y) represents a good which absorbs only a small portion of consumers’ budgets. (z

The law of supply is graphically exhibited by the supply curve which is: (1) Moving all along the demand curve. (2) Vertical. (3) Upward-sloping. (4) Downward-sloping. Can someone please help me in finding out the

Elucidate briefly business cycles and what role do the Federal Government and Federal Reserve has in trying to manage them?

I have a problem in economics on Stockholders of a big business corporation. Please help me in the following question. The stockholders of a big business corporation: (1) Frequently manage the everyday output decisions. (2) Usually own big percentages of the total sha

State the main function of money in economy? Answer: The major function of money in an economic system is to ease the exchange of services and goods.

Most of the mass advertising is planned to: (1) Give accurate information on product and price quality. (2) Boost output to conform to the consumer preferences. (3) Alter the consumer preferences. (4) Provide free TV entertainment and remain newspaper

Can someone please help me in finding out the accurate answer from the following question. When tortilla chips go on sale for fifty percent off, then the demand for salsa is most probable to: (1) Stay similar. (2) Reduce. (3) Raise. (d) Raise only when salsa as well g

Innovation: (w) entails financial investment to create human capital. (x) comprises the commercial introduction of a new product or production process. (y) can reasonably describe only normal accounting profit. (z) was used by John Maynard Keynes to d

Refer to the following domestic production possibilities curve for Karalex. The gain to Karalex from specialization and international trade is represented by a move from: 1) A to B. 2) C to A. 3) C to D. 4) B to E. Discover Q & A Leading Solution Library Avail More Than 1439854 Solved problems, classrooms assignments, textbook's solutions, for quick Downloads No hassle, Instant Access Start Discovering 18,76,764 1923151 Asked 3,689 Active Tutors 1439854 Questions Answered Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!! Submit Assignment

18,76,764

1923151 Asked

3,689

Active Tutors

1439854

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!