Question 1 Manufacturing Cost Schedule and Income Statement

Puss in Boots Pet Food is a wholly owned subsidiary of Jupiter Australia and New Zealand and utilises a traditional manufacturing cost flow inventory and accounting system. Puss in Boots Pet Food is incorporated and operates in Australia, and pays tax at the Australian corporate rate of 30%. Trading data for Puss in Boots Pet Food for the 2014 financial year was as follows and there are no adjustments for accruals or prepayments:

|

Account:

|

$

|

|

Purchases of Raw Materials & Packaging

|

4,628,000

|

|

Factory Overhead

|

1,422,000

|

|

Heat Light & Power Costs (Factory)

|

1,756,000

|

|

Heat Light & Power Costs (Admin)

|

226000

|

|

Depreciation of Factory Plant, Equipment & Machinery

|

1,000,000

|

|

Depreciation of Office Equipment & Furniture

|

38,000

|

|

Office Salaries and Costs

|

76,000

|

|

Factory Direct Labour Cost

|

1,728,000

|

|

Factory Indirect Labour Cost

|

303,000

|

|

Interest & other charges

|

900,000

|

|

Sales Revenue

|

22,101,000

|

|

Freight Outwards

|

172,000

|

|

Freight Inwards

|

55,000

|

|

Sales & Marketing Expenses

|

2,385,000

|

|

Accounting & Audit costs

|

426,000

|

On June 30th 2014 selected account balances of Puss in Boots Pet Food were as follows (with comparative 1/7/2013 Opening Balance figures):

|

Account:

|

Jul 1, 2013

|

Jun 30, 2014

|

|

Work in Process (WIP) Inventory:

|

Opening

|

Closing

|

|

Raw Materials

|

352,000

|

302,000

|

|

Direct Labour

|

39,000

|

35,000

|

|

Manufacturing Overhead

|

96,000

|

86,000

|

|

|

|

|

|

Jul 1, 2013

|

Jun 30, 2014

|

|

Raw Material Inventory

|

156,000

|

178,000

|

|

Finished Goods Inventory

|

942,000

|

1,107,000

|

Required:

Using Excel, prepare a Schedule of Cost of Goods Manufactured, Schedule of Cost of Goods Sold, and an income statement for Puss in Boots Pet Food from the information provided.

Note: Your Excel model should include a data input section and appropriate formulae. An example of Manufacturing Cost Schedules can be found in the Langfield-Smith text on p.58 and an Excel example is available in Resources on the subject Interact site.

Question 2 Strategic Management Accounting Case Study

This question builds on prior studies of Cost Volume Profit (CVP) analysis and relates to learning material and objectives from Online Modules 1 and 2.

(For assistance on how to answer this question you are advised to undertake the case study from Mars Petcare which is provided online in Module 2 as the Topic Reflection Task).

'Friend' Dog Food

STRATEGIC MARKET ANALYSIS

You have joined the cross-discipline Strategic Management Committee of Jupiter Australia as the management accounting representative. The key issue facing this top level management committee at the moment is how to improve profitability in several key product categories across several divisions.

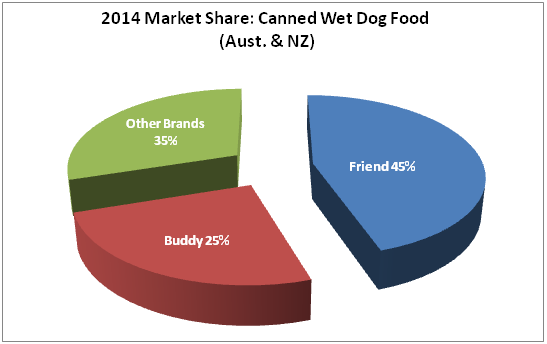

The product currently under discussion is the 'Friend' line of wet dog food sold by Jupiter through the major supermarket chains in Australia and New Zealand. The 'Friend' product has been a market leader for Jupiter Pet Food however lately it has come under increased price competition and the sales and market share of 'Friend' canned dog food have fallen dramatically. The 'Friend' product is marketed as a premium product for large dogs and is priced at a premium to reflect its quality. The major competition comes from a similar product manufactured by a multinational rival branded as 'Buddy' which is also marketed as a premium product, but which sells at a discount to our product the market leader 'Friend'.

The Marketing Department for the Jupiter Dog Food Division has provided the following information about the canned dog food market during the 2014 financial year. The total sales of canned dog food in the Australia and New Zealand market for 2014 was 720 million individual units of which 'Friend' held 45% and 'Buddy' held 25%:

The Marketing Department advises you that at the end of the previous 2013 financial year 'Friend's' market share had been 55% and the 'Buddy' brand held only 15%. Since that time 'Buddy' dog food has been advertising heavily and aggressively pricing their product in the market, increasing their market share to the current level of 25%. The Strategic Management Committee agrees with the marketing department that this sales trend is damaging and is impacting on the profitability of Jupiter's marquee pet food brand 'Friend'. Currently the Return on Total Assets (ROTA) for Friend dog food has fallen to 24.92% (calculated by dividing Gross Profit by Total Assets). This is marginally below the required ROTA of Jupiter which is 25%. If the product continues to lose market share it may not be viable.

As the Management Accounting representative you have provided the Strategic Management Committee with the following breakdown of revenues and costs for the 'Friend' product line for the just completed 2014 financial year:

|

Friend Dog Food

|

|

|

Total Assets 'Friend' Factory

|

$65m

|

|

Total Sales (Volume in Units)

|

324m

|

|

Regular Retail Price (per unit retail price)

|

$2.99

|

|

Gross Sales Value Received (per unit wholesale price)

|

$2.35

|

|

Supermarket Rebates (per unit)

|

$0.15

|

|

Net Sales Value Received (per unit)

|

$2.20

|

|

Prime Costs (per unit)

|

$0.55

|

|

Other Manufacturing Costs (per unit)

|

$1.00

|

|

Logistic Costs (per unit)

|

$0.60

|

|

Gross $ Margin (Gross Profit) (per unit)

|

$0.05

|

|

Total $ Margin (Gross Profit)

|

$16.2m

|

|

% Return on Total Assets (ROTA)

|

24.92%

|

The Marketing Department has carried out research into the wet dog food market which indicates that by discounting the recommended retail price of 'Friend' by $0.24 per unit to $2.75 per unit*, unit sales of 'Friend' will increase by 15%. In an attempt to simultaneously lower 'Friend' product costs the research and development (R&D) team have identified that by slightly altering the meat and cereal ingredients quality and mix a saving of 15% of prime costs can be made.

However, the Chair of the Strategic Management Committee advises that even after allowing for the 15% savings in prime costs, discounting the product by $0.24 per unit will mean that the product will no longer achieve the firm's long term required return on total assets (ROTA) of 25%,. The CEO argues that if this remains the case, the previously successful 'Friend' product line may have to be discontinued.

You advise the Committee that you are aware that the 'Friend' manufacturing facility in Wodonga is currently running at 71% of its practical capacity and that the warehouse facility (logistics) is running at 68% capacity. You are also aware that whilst the 'Friend' product's Prime Costs are 100% Variable, other Manufacturing Costs and Logistic Costs are made up of 75% Fixed costs and 25% Variable costs.

It can be assumed that this cost break-down between variable and fixed costs will hold consistently across the industry (including for competitor Buddy). Assume that 80% of the predicted 'Friend' unit sales increase will be made at the expense of the unit sales of their main competitor 'Buddy' meaning 'Buddy' sales will fall by 80% of the 'Friends' sales increase. Finally, assume that 'Friend' and 'Buddy' have identical cost structures at the commencement of the 2015 financial year, prior to the recommended changes.

You ask if you can be given time to prepare a report for the Strategic Management Committee on the Management Accounting cost and profit implications of the changes proposed by Marketing and R&D based on the budgeted costs and increases in sales and production.

*Remember that the manufacturer does not receive the retail price. The discounted wholesale price will be $2.11 per unit, down from $2.35 per unit.

Required:

(i) Using excel prepare a 'before and after' budget comparative analysis of the revenues and costs of the 'Friend' product line. The analysis should incorporate the $0.24 cent drop in price, the 15% predicted savings in prime costs, and include the 15% predicted sales increase. Ensure you include in your analysis any impact of the budgeted production increase on other per unit manufacturing and logistics costs.

(ii) Prepare a brief report (approx. 300 words) for the Strategic Management Committee outlining the key points of your findings. Include some discussion on:

a. the likely impact of the changes on the cost and profit structure of Friend Dog Food Division (derived from your answer to (i)).

b. Calculate and discuss the likely impact of the changes on the cost structure of our main competitor Buddy Dog Food (use Excel).

c. Make a recommendation to the Committee on whether to go ahead with the planned changes. Include any other strategic advice that you consider relevant to the Committee's decision making.

Question 3 Comprehensive Manufacturing Budget

This question builds on prior studies and relates to learning material and objectives from Online Modules 1, 2 and 3. Links to specific resources provided for this question relating to Manufacturing Budgets and Excel spreadsheets can be found in the Online Topic Modules.

You have been asked to prepare a 5 year budget forecast for the 'Giggles' Chocolate and Nut Nougat Energy Bar factory.

The 'Giggles' division of the Neptune Australia company utilises a traditional manufacturing cost flow inventory and accounting system.

As at June 30th 2014 the following financial and trading data was provided:

|

2014 Year data (all costs are per unit)

|

|

|

Sales (Units)

|

102.36 million

|

|

Price (average 2014 price received)

|

$0.956

|

|

|

|

Prime Costs (per unit)

|

|

|

Ingredients (including chocolate and nuts)

|

$0.1950

|

|

Direct Labour

|

$0.0250

|

|

Variable OH Manufacturing Costs (per unit)

|

$0.3400

|

|

Factory Management Salaries (per annum)

|

$725,000

|

|

Factory Plant & Equipment Depreciation (per annum)

|

$500,000

|

|

Sales and Marketing Costs (per annum)

|

$5,186,000

|

|

Finance Costs (per annum)

|

$1,465,500

|

|

Non-Factory Administration Costs (per annum)

|

$764,000

|

|

Inventory on Hand (at valuation):

|

|

|

Ingredients & Packaging (2,001,500 units)

|

$410,000

|

|

Finished Goods (2,020,500 units)

|

$1,150,000

|

'Giggles' maintains a target safety stock of raw materials inventory and finished goods inventory amounting to the equivalent of one (1) week of the current year's budgeted unit sales. At the end of the 2014 financial year there were 2,020,500 completed units of 'Giggles' chocolate bars in the warehouse as Finished Goods. There was enough raw materials on hand to manufacture 2,001,500 units of 'Giggles' chocolate bars.

Management at 'Giggles' predict that unit sales of the company's chocolate bar will continue to grow indefinitely at a rate of 4% above the 2.25% current long term rate of inflation (budgeted 6.25% increase per annum). The company is budgeting to achieve a year on year price increase of 1% over the long term inflation rate (3.25% annual increase). Factory Depreciation expense is straight line at $500,000. All other costs including direct labour and ingredient costs are expected to increase annually at the rate of inflation. The company pays tax at the Australian Corporate tax rate which is expected to hold at 30%. The inflation rate of 2.25% is expected to hold over the 5 year budget period.

The 'Giggles' factory has been operating at its current site in Ballarat, Victoria since the late 1970s, however due to the consistent growth in sales of the 'Giggles' chocolate bar, the factory is nearing its practical manufacturing capacity of 110 million chocolate bars per annum.

Required:

(i) Using Excel develop a Sales, Production and Purchase budget as well as a budgeted Schedule of Cost of Goods Manufactured, Schedule of Cost of Goods Sold, and an Income Statement for each of the 5 years in the budget period (commencing July 1, 2014) (advice on the form of these budgets is linked through the online topic modules and in the Interact Resources folder and is also available in the Appendix to Chapter 9 of the text book). This budget must also take into account the manufacturing facility practical capacity production constraint. Your spreadsheet must include a data section which enables inputs (such as the inflation rate, budgeted cost and sales increases, and the production limit) to be simply altered and 'what if' analysis to be undertaken. (Excel resources are provided on your Interact site to guide students on the use of the 'IF' formula which can be used for the budget production constraint).

Hint: All 5 years of each budget should be shown side by side (1 column per year) for ease of comparison by management. All of the budgets should be presented on one worksheet together, working down the page commencing with the Sales and then Production budgets.

You should be able to drag the formula across for the whole of the budget if the first years are properly constructed with a data input section and using absolute referencing. This makes the process much quicker and easier. An Excel help file and video which deals with the formula required has been placed in the Resources folder in the subject Interact site to assist students (linked through Online Module 3).

(ii) The CEO of 'Giggles' is aware of the impending production problems caused by the 110 million unit practical manufacturing capacity of the factory. The CEO faces the option of trying to limit costs and maximise profit within the current manufacturing and sale constraint or invest in new plant to expand the capacity of the factory. An investment in new plant will cost $12 million in new plant and increase the current manufacturing capacity by 20%. It will have no impact on any variable costs or on other manufacturing costs. It is expected that this new factory plant would be depreciated straight line to zero over 20 years. The planned upgrade can be completed and ready for operation by the commencement of the 2016 financial year.

Using the excel model developed in part (i) calculate the impact on sales and profit if the option of upgrading the manufacturing facility is exercised and the practical production capacity of the factory is increased by 20% (Include the additional factory depreciation expense. Submit results as a separate worksheet).

(iii) Given your findings from part (i) and (ii) write a report for the CEO of 'Giggles' recommending whether to take up the option to upgrade the production facility. In your report consider all of the strategic and financial implications to the firm of reaching its production constraint and any implications or opportunities arising from upgrading the facility and having extra productive capacity. Your grade will depend on the accuracy and depth of your analysis, and your capacity to identify strategic issues which management should consider when making their decision.

Question 4

This question relates to learning material and objectives from Online Module 5.

The Jupiter Australia factory in Albury Wodonga responsible for manufacturing high end cat food products for export into the Japanese market operates continuously 24 hours a day, 7 days a week. The factory employs a process costing system. As a management accountant for the Pet Food Division of Jupiter Australia you are required to produce end of period product costing for a range of different product lines including the 'Sashimi' export cat food trays. The 'Sashimi' product is a blend of sea food and cereal which is mixed and then cooked in a sealed aluminium tray.

The process for manufacturing 'Sashimi' is to first mix all of the ingredients. The mixed ingredients are then sealed in the aluminium tray and pressure cooked. It is assumed for Process Costing purposes that all Raw Material ingredients and packaging are added at the commencement of the process. For the purpose of accounting, the conversion costs of manufacturing are assumed to occur evenly across the whole of the production cycle which takes several hours.

The following information relates to the production of 'Sashimi' during the month of June 2014.

|

Work-in-Process: June 1, 2014

|

35,286 Units

|

|

|

Stage of completion

|

Value

|

|

Raw materials

|

100%

|

$18,750

|

|

Conversion

|

65%

|

$17,200

|

|

|

|

|

Work-in-Process: June 30, 2014

|

87,540 Units

|

|

|

30% Complete

|

A total of 2,926,100 individual trays of Sashimi cat food were completed during June and the following costs were incurred.

|

Costs incurred during June 2014:

|

|

Raw materials

|

$1,554,500

|

|

Conversion

|

$2,243,100

|

Required:

(i) Using the Weighted Average Cost Method determine the cost value of closing WIP and the cost value of goods transferred out during the period.

(ii) Using the First In First Out (FIFO) method determine the cost value of closing WIP and the cost value of goods transferred out during the period.

Question 5 Activity Based Costing (ABC)

This question relates to learning material and objectives from Online Module 6.

Banzai is a range of aluminium foil tray premium dog food products manufactured for export to Japan from one of several pet food factories based at Jupiter Australia's head office location in Wodonga, Victoria.

Banzai manufactures a Standard range of products and an Advanced range. The Advanced range uses slightly more expensive ingredients and involves the process of adding a small premium food display item to the top of each individual tray of pet food. The Advanced product sells in much smaller numbers than the Standard product and consequently has smaller batch runs when processing. The Standard model wholesales for AUD $1.50 whilst the Advanced product model sells for AUD $2.5. Currently the cheaper Standard product outsells the more expensive Advanced product at a rate of 10 to 1.

The Banzai factory uses a normal costing approach to allocate overhead costs to products. The cost driver used is machine hours which recognises the amount of machine time expended in the manufacture of each unit. The Managing Director of the Banzai product line has reviewed the comparative margins earned on the two products using the following data:

|

2015 Sales and Cost estimates

|

Standard Product

|

Advanced Product

|

|

Forecast Sales (Units)

|

12,000,000

|

1,200,000

|

|

Selling price per unit($)

|

$1.50

|

$2.50

|

|

Prime Costs per unit

|

$0.50

|

$0.80

|

|

Machine Hours per 1,000 Units

|

1

|

1

|

The firm has always applied overhead to product costs based on Machine Hours as the factory-wide cost driver. For 2015 it is expected that OH will be applied to each product at the rate of $500 per machine hour.

The Managing Director and Marketing Manager believe that the Gross Profit on sales of the Advanced product are achieved at a higher margin than the Standard product and therefore more focus should be placed on manufacturing and selling the Advanced product. Whilst the Standard Bonzai product is superior to others on the market it has been slowly losing market share to slightly cheaper competitors. Because of its perceived lower margin the company does not believe that it is sustainable to discount the Standard product to meet competitors. The Marketing Manager believes it is time for the firm to focus on the more profitable niche market for the Advanced product.

Whilst you are relatively new to the Banzai manufacturing team you have noticed that it takes a considerable amount of set up time to re-gear the automated machines to place the different premium food display items for the Advanced product. You have also noted that the manufacturing batch size for the Advanced product is much smaller and so requires more frequent set up and that quality checking is conducted on 0.25% of units for the Advanced product compared to 0.05% of the Standard product. You are not convinced that the traditional approach to applying overhead is appropriate and you decide to prepare a report comparing the two products comparing product costing using the current factory-wide OH allocation approach compared with Activity Based Costing techniques using the following overhead cost data:

|

Activity

|

Cost

|

Cost Driver

|

Amount of Cost Driver

|

|

Standard

|

Advanced

|

|

Machining Set Ups

|

$2,475,000

|

Set up Hours

|

400

|

500

|

|

General maintenance

|

$1,749,000

|

Machine Hours

|

12,000

|

1,200

|

|

Quality Control

|

$1,350,000

|

QA Samples per 10,000 units

|

6,000

|

3,000

|

|

Packing

|

$1,026,000

|

Number of Orders

|

1000

|

200

|

|

Total Activity Costs

|

$6,600,000

|

|

|

|

Required:

(i) Using the current factory-wide cost driver method of applying overhead at Bonzai develop a spreadsheet to calculate for each product the expected:

i. Gross Profit per unit,

ii. Gross Profit margin ($GP/$Sales),

iii. Total Gross Profit per Model, and

iv. Total Firm Gross Profit.

(ii) Using the activity cost data provided conduct the same analysis utilising Activity Based Costing techniques to again calculate for each model the expected:

i. Gross Profit per unit,

ii. Gross Profit margin ($GP/$Sales),

iii. Total Gross Profit per Model, and

iv. Total Firm Gross Profit.

(iii) Write a brief report outlining your findings and making a recommendation to the management of Banzai about the profitability of the two products and the firm's current costing practices. Discuss the currently falling sales of the Bonzai Standard product and propose a strategic response given your findings above.

Question 6

This question relates to learning material and objectives from Online Module 1.

Pluto Pasta is a wholly-owned subsidiary of Jupiter Australia which manufactures a wide range of packaged food products which are sold through supermarkets. The company has a management bonus system which is based in part on whether reported profit exceeds budgeted profit. Over the past 10 years the bonus of almost 10% of annual salary has been paid every year. Over this period the management staff at Pluto Pasta have come to treat the bonus as a 'normal' part of their remuneration and expect to receive it every year.

Nathan Swan is a fellow accounting graduate employed by the Jupiter Group at the same time as you and he is now a management accountant at Pluto Pasta. His immediate supervisor is the Factory Accountant Marcus Hawk. After several conversations with the CEO and other senior managers at Pluto Pasta Marcus is feeling significant pressure to maintain the bonuses by ensuring that reported profit remains at a high level in comparison to budget.

Over many years Factory Accountant Marcus has developed a close relationship with Docker Ltd who perform repairs and maintenance on Pluto's production lines and ovens. In the previous year Docker billed service fees of more than $8 million to Pluto's repair and maintenance expense. Concerned that Pluto will not meet its profit targets in the current year Marcus Hawk approaches his contacts at Docker Ltd and asks them to invoice 50% of the current year's $8.5 million repair and maintenance expense budget as purchases of production plant and equipment. This will mean that $4.25 million of expense will be classified as assets and will increase reported profit. To maintain a good relationship with Hawk and Pluto Pasta who are their largest customer Docker Ltd agree to the request.

Your friend the management accountant Nathan Swan noticed the overall decreased levels of repairs and maintenance expense and also the increased purchases of equipment from Docker ltd. He reported the discrepancies to his line manager in Marcus Hawk who told him "it was an accounting treatment that, in the long run, had no overall impact on profitability". Hawk warned Swan not to get involved.

Required:

(i) Swan has come to you as a professional colleague asking for your guidance. What advice would you provide him about the ethics of Hawk's actions?

(ii) What action would you recommend Swan take (explain your reasoning)?

As a starting point to assist in answering this question please refer to the appendix of Chapter 1 of the Langfield-Smith et al text and also the APES GN 40 Ethical Conflicts in the Workplace - Considerations for Members in Business PDF prepared by the Accounting Professional & Ethical Standards Board which is provided on the subject Interact site (linked through Online Module 1). Students are expected to also conduct their own research outside the text and Online Module materials in order to respond to this case study.