Assignment:

Question 1

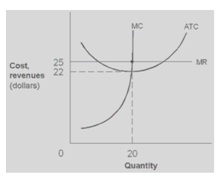

Exhibit 8-7 A firm's cost and MR curves

In Exhibit 8-7, if this firm is currently producing 20 units of output, this firm:

a. should shut down.

b. is losing $20.

c. is earning a total profit of $60.

d. is earning a total profit of $3.

e. is at its profit-maximizing point.

Question 2 If resource prices rise and the per-unit cost of producing a product increases as the firms in an industry expand output in response to an increase in demand, the long-run market supply curve for the product will:

a. be more inelastic than the short-run supply curve for the product.

b. be perfectly inelastic (a vertical line).

c. slope upward to the right.

d. be perfectly elastic (a horizontal line).

Question 3 If a perfectly competitive firm sells 50 units of output at a market price of $10 per unit, its marginal revenue is:

a. $5300.

b. $10.

c. more than $10.

d. less than $10.

Question 4 Assume that a firm's marginal revenue just barely exceeds marginal cost. Under these conditions the firm should:

a. maintain output.

b. expand output.

c. There is insufficient information to answer the question.

d. contract output.

Question 5 In the perfectly competitive market, individual firms exert no effect on the market price. Therefore, the firm's marginal revenue curve is:

a. indeterminate.

b. the same as the firm's demand curve.

c. a downward-sloping curve.

d. an upward-sloping curve.

Question 6 In short-run perfectly competitive equilibrium, which of the following is alwaystrue?

a. Profit is positive, otherwise firms would not produce.

b. Profit can be zero or positive, but not negative.

c. Profit can be negative, zero, or positive.

d. Profit equals zero.

Question 7 In the short run, a perfectly competitive firm's most profitable level of output is where:

a. marginal cost exceeds marginal revenue.

b. total revenue is at a maximum.

c. marginal cost equals marginal revenue.

d. All of these.

Question 8 If a firm is operating at a loss in the short run and finds that its price is greater than average variable cost, then in the short run:

a. total revenue is greater than total costs.

b. it should produce where MR = MC.

c. it should go out of business.

d. it should produce zero output.

e. total revenue is less than total variable costs.

Question 9 Suppose product price is fixed at $24; MR = MC at Q = 200; AFC = $6; AVC = $16. What do you advise this firm to do?

a. Decrease output.

b. Increase output.

c. Stay at the current output; the firm is earning a profit of $400.

d. Stay at the current output; the firm is losing $200.

e. Shut down operations.

Question 10 If a firm's marginal revenue from its 100th unit of output is $50 and the marginal cost from its 100th unit of output is $45, then in the short run this firm should:

a. produce less than 100 units of output.

b. shut down.

c. change its technology.

d. increase its plant size.

e. produce more than 99 units of output.

Question 11 What should a profit maximizing monopolist do if she is currently producing where MC < MR?

a. Shut down in the long run.

b. Decrease output until MC = MR.

c. Operate only in the short run.

d. Increase output until MC = MR.

e. Keep producing at this level.

Question 12 A monopolist always faces a demand curve that is:

a. the same as the entire market demand curve.

b. perfectly elastic.

c. unit elastic.

d. perfectly inelastic.

Question 13 If pizza used to be produced in a perfectly competitive market, and now the pizza market has become a monopoly, we can expect:

a. more pizza to be sold at a lower price.

b. less pizza to be sold at a higher price.

c. more pizza to be sold at a higher price.

d. less pizza to be sold at a lower price.

e. the same amount of pizza to be sold at the same price.

Question 14 Suppose a monopolist charges a price corresponding to the intersection of the marginal cost and marginal revenue curves. If this price is between its average variable cost and average total cost curves, the firm will:

a. earn an economic profit.

b. stay in operation in the short-run, but shut down in the long run if demand remains the same.

c. shut down.

d. none of these.

Question 15 For a monopolist with a downward-sloping demand curve,

a. the coefficient of price elasticity of demand is zero.

b. when the price is equal to zero, marginal revenue is equal to zero.

c. as price decreases, marginal revenue decreases.

d. the coefficient of price elasticity of demand is infinite.

e. as price increases, marginal revenue decreases.

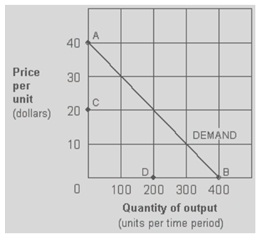

Question 16 Exhibit 9-1 Monopolist's demand curve

Which of the following points in Exhibit 9-1 would not lie on the marginal revenue curve corresponding to the monopolist's straight-line demand curve?

a. C.

b. C and B.

c. A.

d. B.

Question 17 Which of the following statements best describe the price, output, and profit conditions of monopoly?

a. Price will equal marginal cost at the profit-maximizing level of output and profits will be positive in the long-run.

b. Price will always equal average variable cost in the short-run and either profits or losses may result in the long run.

c. In the long-run, positive economic profit will be earned.

d. All of these are true.

Question 18 The monopolist, unlike the perfectly competitive firm, can continue to earn an economic profit in the long run because of:

a. cartels.

b. price leadership.

c. collusive agreements with competitors.

d. a dominant firm.

e. extremely high barriers to entry.

Question 19 An industry in which total costs are kept to a minimum because only one firm serves the whole market is called a:

a. patent monopoly.

b. natural monopoly.

c. competitive monopoly.

d. limit monopoly.

Question 20 The act of buying a commodity in one market at a lower price and selling it in another market at a higher price is known as:

a. buying long.

b. selling short.

c. arbitrage.

d. a tariff.

Question 21 Which of the following explains how a cartel with 100 percent control might raise price to monopoly-like levels?

a. By setting a group output level equal to a profit-maximizing monopolist, and then assigning binding quota shares to cartel members.

b. By forbidding price competition, but allowing non-cooperative rivalry in output levels.

c. By setting an official price that members can secretly undercut.

d. None of the above.

Question 22 If a monopolistically competitive firm can earn a profit, it will increase production until:

a. MR > AVC.

b. MR = AR.

c. MR = MC.

d. MR = ATC.

e. MC > MR.

Question 23 Which of the following best describes a cartel?

a. A group of identical non-cooperative oligopolists that are able to reproduce a monopoly equilibrium through price rivalry.

b. As a monopolist, a group of monopolistically competitive firms that jointly reduce output and raise the price.

c. As a monopolist, a group of cooperating oligopolists that jointly reduce output and raise the price.

d. A monopolist that reduces output and raises price.

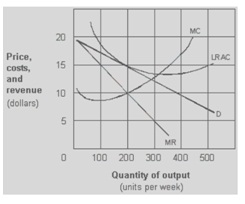

Question 24 Exhibit 10-2 A monopolistic competitive firm

As presented in Exhibit 10-2, the long-run profit-maximizing output for the monopolistic competitive firm is:

a. 400 units per week.

b. zero units per week.

c. 300 units per week.

d. 100 units per week.

e. 200 units per week.

Question 25 Which of the following is evidence of an ineffective cartel?

a. Output changes are dictated by changes in demand.

b. Price changes are dictated by changes in demand.

c. Members do not agree on output quotas.

d. All of these.

Question 26 Which of the following statements best describes firms under monopolistic competition?

a. Profits will be positive in the long run.

b. Price always equals average variable cost.

c. In the long run, positive economic profit will be eliminated.

d. Marginal revenue equals minimum average total cost in the short run.

Question 27 When Pepsi is considering a price hike, it needs to consider how Coke may react. This situation is called:

a. monopolistic competition.

b. mutual interdependence.

c. price leadership.

d. collusion.

Question 28 Perfect competition and monopolistic competition are similar because under both market structures,

a. there are zero economic profits in the long run.

b. differentiated products are produced.

c. there are few firms.

d. entry is difficult.

e. production takes place at the least-cost combination.

Question 29 For a kinked demand curve, the marginal revenue curve is:

a. a vertical line.

b. above the demand curve.

c. a horizontal line.

d. positively sloped.

e. discontinuous.

Question 30 The theory of monopolistic competition predicts that in long-run equilibrium a monopolistically competitive firm will:

a. produce the output level at which price equals long-run average cost.

b. produce the output level at which price equals long-run marginal cost.

c. operate at minimum long-run average cost.

d. overutilize its insufficient capacity.

Question 31 The demand curve in monopolistic competition slopes downward because of:

a. government regulation.

b. the small number of firms.

c. strong barriers to entry.

d. the similarities of the businesses.

e. product differentiation.

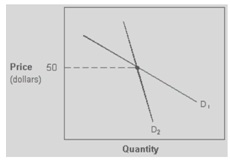

Question 32 Exhibit 10-4 Kinked demand curves

In Exhibit 10-4, the exhibit represents a kinked-demand oligopoly model. Suppose the current price is $50. If one firm in the oligopoly now attempts to raise price, all firms will:

a. lower their prices.

b. follow along demand curve D2.

c. ignore this price increase and cause the price-raising firm to move along D

d. follow along demand curve D

e. ignore this price increase and cause the price-raising firm to move along D2.

Question 33 Which of the following is not true about a monopsonist?

a. It is the only buyer of labor in a market.

b. It determines the optimal employment-wage rate combination by equating the marginal revenue product of labor to the marginal cost of labor.

c. It can set the wage rate and hire any desired number of workers at that wage.

d. It usually has to bargain with unionized workers.

e. It usually extracts rents from its monopsony power.

Question 34 In a monopsonistic labor market, workers are paid a wage:

a. equal to the MFC.

b. equal to the price of the output.

c. equal to the intersection of MRP and S.

d. above their MFC.

e. below their MRP.

Question 35 Which of the following statements is true?

a. The demand curve for a perfectly competitive employer is horizontal at the market wage rate.

b. Marginal revenue product is the extra revenue generated to the firm from the production of one more unit of output.

c. The supply curve of labor is upward sloping because of the law of diminishing marginal productivity.

d. Marginal factor cost is the extra cost to a firm of employing one more unit of a factor of production.

Question 36 A monopsony is a:

a. single buyer.

b. large seller.

c. large number of buyers.

d. single seller.

Question 37 For a monopsonist, the marginal factor cost is always:

a. less than the wage rate.

b. equal to the wage rate.

c. the same as the labor supply.

d. greater than the wage rate

e. the same as the labor demand.

Question 38 Exhibit 11-14 Labor cost data for a monopsonist

|

Wage Rate

|

Number of

Workers

|

|

$ 0

|

0

|

|

5

|

10

|

|

8

|

20

|

|

12

|

30

|

|

16

|

40

|

In Exhibit 11-14, the monopsonist will maximize profits by hiring how many workers?

a. 20.

b. Unable to determine from the information given.

c. 30.

d. 40.

e. 10.

Question 39 Marginal revenue product is defined as the extra:

a. revenue earned by hiring one more unit of resource

b. output a firm would receive after hiring one more unit of resource.

c. cost of hiring one more unit of resource

d. revenue earned by selling one more unit of product.

e. output received by spending one more dollar on resources

Question 40 For a competitive firm, workers' marginal revenue product equals the marginal product of labor times the:

a. firm's total revenue.

b. interest rate.

c. price of the firm's product.

d. wage rate.