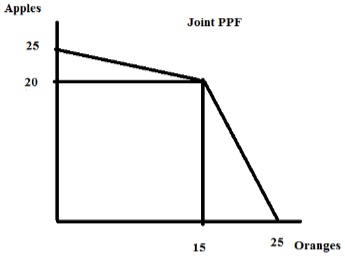

Problem 1. Use the following graph to answer this question. The graph shows a joint PPF for Bob and Jane who both produce apples and oranges. You are told that Bob has the comparative advantage in producing apples.

a. Given the above graph, are the following points feasible, inefficient, or not feasible?

i. (18 oranges, 15 apples) _______

ii. (19 oranges, 10 apples) _______

b. What is Bob's opportunity cost of producing an additional four apples? Be sure to provide a unit of measurement in your answer! _________

c. What is Jane's opportunity cost of producing an additional three oranges? Be sure to provide a unit of measurement in your answer! _________

Problem 2. [Multiple Choice Question here!] Suppose that you know that the market for good Y is initially in equilibrium. Then, you are told that the number of firms in the industry that produce good Y decrease while at the same time people's incomes increase in this economy. Given this information, which of the following statements is true:

a. We know with certainty that the equilibrium price of good Y is indeterminate irrespective of whether good Y is a normal or an inferior good.

b. We know with certainty that the equilibrium price of good Y is indeterminate if good Y is an inferior good.

c. We know with certainty that the equilibrium quantity of good Y is indeterminate irrespective of whether good Y is a normal or an inferior good.

d. We know with certainty that the equilibrium price of good Y is indeterminate if good Y is a normal good.

Problem 3. Consider a market in which there are ten consumers of the good. Five of these consumers have identical demand curves that can be expressed as follows:

Individual demand curve: P = 10 - Q

An additional five consumers have identical demand curves that can be expressed as follows:

Individual demand curve': P = 5 - Q

In these equations P is the price per unit and Q is the quantity of units demanded. Given this information, what is the equation for the market demand curve? Make sure you identify the relevant domain or range for the market demand curve.

Problem 4. Consider the small, closed economy of Utopia's market for gadgets. The following equations give you the domestic demand and domestic supply curves for this market where P is the price per gadget and Q is the quantity of gadgets:

Domestic Demand for Gadgets: P = 100 - 2Q

Domestic Supply of Gadgets: P = 20 + 3Q

You are also told that the world price of gadgets is $32 per gadget.

Suppose this market is open to trade while at the same time an import quota of 15 units is imposed. Given this information and holding everything else constant, answer the following questions. Show your work so that Anton can see how you found your answer!

i. How many gadgets will be demanded in Utopia with this policy?

ii. How many gadgets will be supplied domestically in Utopia with this policy?

iii. What will be the value of consumer surplus in Utopia with this policy?