Objective of the Case study: This case study aims at helping students to reflect on what they learnt throughout the module.

Question 1:

The following financial data (a,b,c) is for three retail businesses, which are listed on the London Stock Exchange.

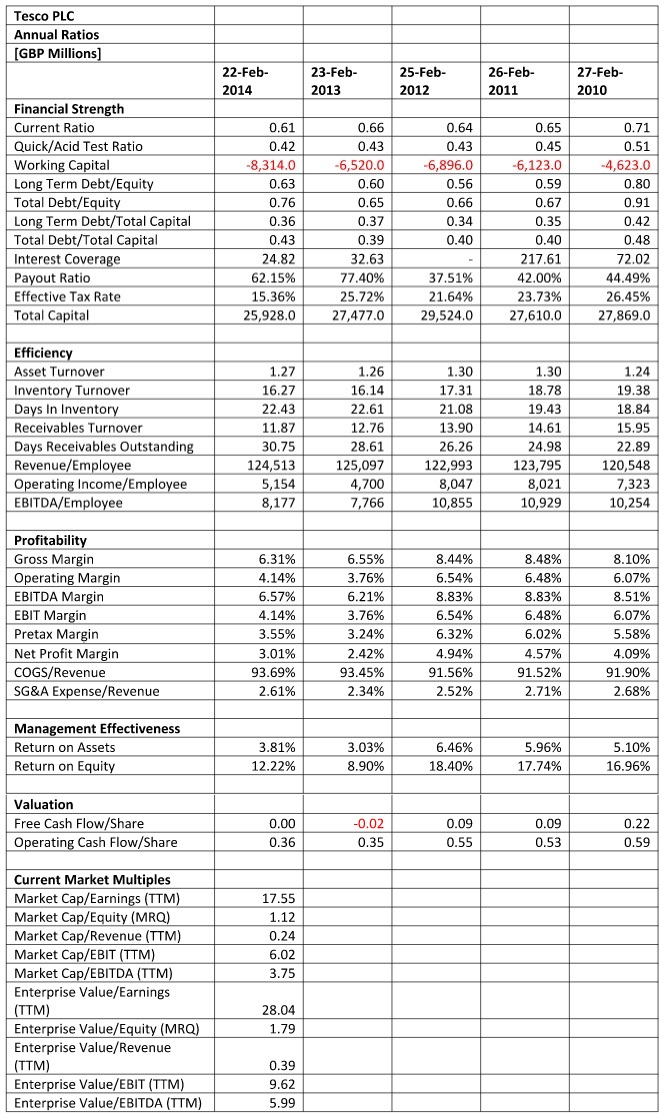

a) Tesco PLC:

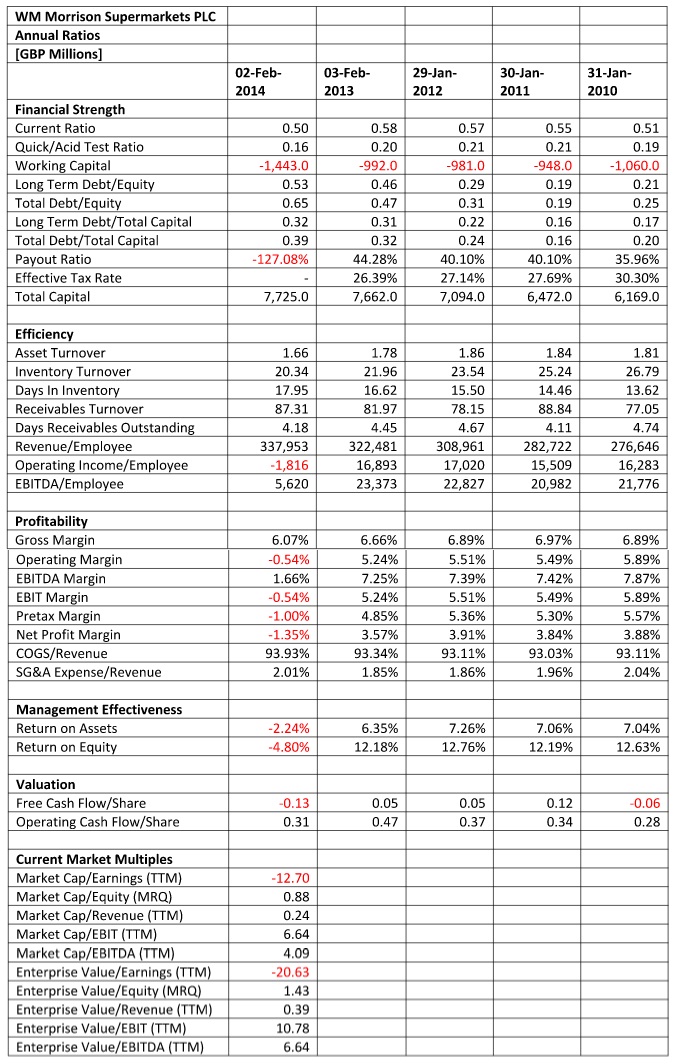

b) Morrisons PLC:

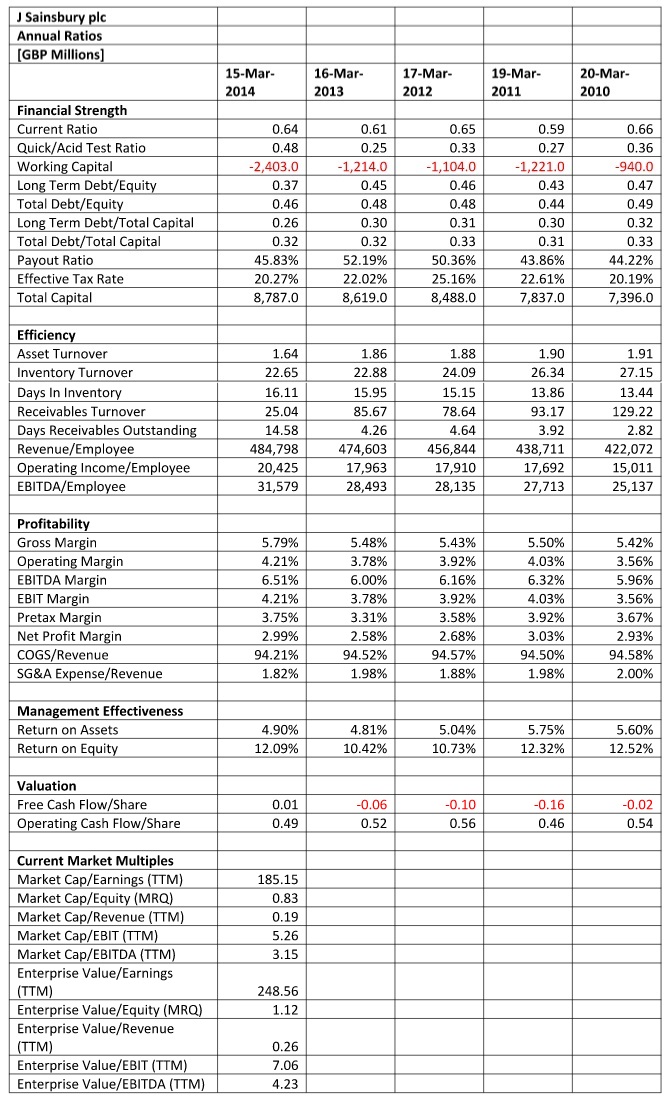

c) Sainsbury PLC:

You are required to:

(a) Select and justify at least 10 financial ratios and calculate 2 non-financial ratios to analyse the performance and financial position of the three companies. You are expected to use charts to compare performance of the three companies. You will need to look at the audited financial statement and carry out further research to explain the performance of the company over the five years. For clarity, you are expected to rank the companies based on the individual benchmarks and overall.

(b) Write a memo to the managing director of the worst performing company with recommendations of how the financial performance of the business can be improved.

(c) Outline the limitations of relying on financial ratios to interpret firm performance?

You are expected to research for more information on the companies and cite the material correctly. You can use the Global Business Browser database to access analysts’ and SWOT reports.

Question 2:

Sound Equipment Ltd was formed five years ago to manufacture parts for hi-fi equipment. Most of its customers were individuals wanting to assemble their own systems. Recently, however, the company has embarked on a policy of expansion and has been approached by JBZ plc, a multinational manufacturer of consumer electronics. JBZ has offered Sound Equipment Ltd a contract to build an amplifier for its latest consumer product. If accepted, the contract will increase Sound Equipment’s turnover by 20%.

JBZ’s offer is a fixed price contract over three years, although it is possible for Sound Equipment to apply for subsequent contracts. The contract will involve Sound Equipment purchasing a specialist machine for £150 000. Although the machine has a 10-year life, it would be written off over the three years of the initial contract as it can only be used in the manufacture of the amplifier for JBZ.

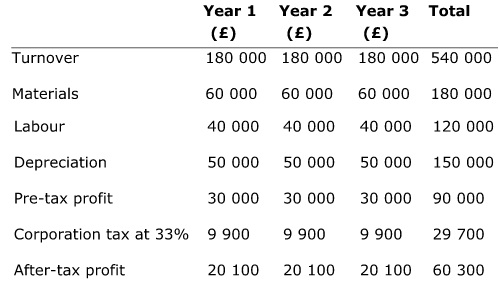

The production director of Sound Equipment has already prepared a financial appraisal of the proposal. This is reproduced below. With a capital cost of £150 000 and total profits of £60 300, the production director has calculated the return on capital employed as 40.2%. As this is greater than Sound Equipment’s cost of capital of 18%, the production director is recommending that the board accepts the contract.

You are employed as the assistant accountant to Sound Equipment Ltd and report to John Green, the financial director, who asks you to carry out a full financial appraisal of the proposed contract. He feels that the production director’s presentation is inappropriate. He provides you with the following additional information:

i) Sound Equipment pays corporation tax at the rate of 33%;

ii) The machine will qualify for a 25% writing-down allowance on the reducing balance;

iii) The machine will have no further use other than in manufacturing the amplifier for JBZ;

iv) On ending the contract with JBZ, any outstanding capital allowances can be claimed as a balancing allowance;

v) The company’s cost of capital is 18%;

vi) The cost of materials and labour is forecast to increase by 5% per annum for years 2 and 3.

John Green reminds you that Sound Equipment operates a just-in-time stock policy and that production will be delivered immediately to JBZ, who will, under the terms of the contract, immediately pay for the deliveries. He also reminds you that suppliers are paid immediately on receipt of goods and that employees are also paid immediately.

Notes:

For the purpose of this task, you may assume the following:

(a) the machine would be purchased at the beginning of the accounting year;

(b) there is a one-year delay in paying corporation tax;

(c) all cash flows other than the purchase of the machine occur at the end of each year;

(d) Sound Equipment has no other assets on which to claim capital allowances.

REQUIRED:

Write a report with recommendations to the financial director. Your report should include:

a) Use the net present value technique to identify whether or not the initial three-year contract is worthwhile.

b) Explain your approach to taxation in your appraisal.

c) Discuss two other investment appraisal methods that could be used to evaluate this project.

d) What others factors would need to be considered before making a final decision.

You are expected to research for theoretical information on investment appraisal techniques and cite the material correctly.

All assumptions made should be clearly stated.

ADDITIONAL GUIDANCE:

1. All calculations must be detailed and presented clearly.

2. Use of published work (citing references) within text is expected.

3. A full list of references should be presented at the end of the case study.

4. Please avoid the use of ‘I, We, Us’ in your case study. You are expected to write in third person.

5. Include the assignment front sheet and marking scheme which is attached to the assignment brief.

6. Your answer should not repeat the question as it will be included in your word count.

7. Formatting:

a. Font Type: Arial.

b. Font size 11/12.

c. Line spacing 1.5 to 2.

d. All pages must be numbered

e. All graphs, charts and tables should have a number and a title.

f. All text must be aligned to the left.

8. Good use of English, referencing and presentation.