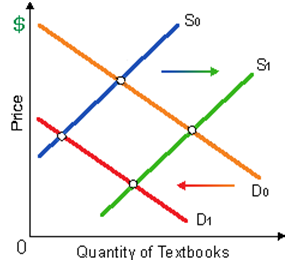

The demand for textbooks has transferred from D0 to D1 whereas supply changed from S0 to S1. Such shifts make sure that the market equilibrium: (w) price will increase. (x) price will fall. (y) quantity will increase. (z) quantity will decrease.

Can someone explain/help me with best solution about problem of economic...