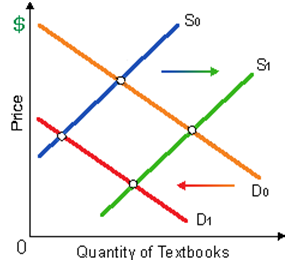

This alters in the supply- and demand-curves for textbooks could not have resulted from a change in: (w) taxes. (x) relative prices for text books. (y) expectations about future prices. (z) prices for related goods.

Hello guys I want your advice. Please recommend some views for above economics problems.