Task 1: Property, plant, and equipment and intangible assets; comprehensive

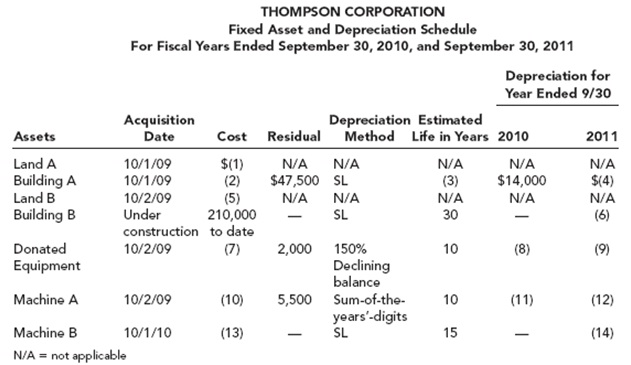

The Thompson Corporation, a manufacturer of steel products, began operations on October 1, 2009. The accounting department of Thompson has started the fixed-asset and depreciation schedule presented below. You have been asked to assist in completing this schedule. In addition to ascertaining that the data already on the schedule are correct, you have obtained the following information from the company's records and personnel:

a. Depreciation is computed from the first of the month of acquisition to the first of the month of disposition.

b. Land A and Building A were acquired from a predecessor corporation. Thompson paid $812,500 for the land and building together. At the time of acquisition, the land had a fair value of $72,000 and the building had a fair value of $828,000.

c. Land B was acquired on October 2, 2009, in exchange for 3,000 newly issued shares of Thompson's common stock. At the date of acquisition, the stock had a par value of $5 per share and a fair value of $25 per share. During October 2009, Thompson paid $10,400 to demolish an existing building on this land so it could construct a new building.

d. Construction of Building B on the newly acquired land began on October 1, 2010. By September 30, 2011, Thompson had paid $210,000 of the estimated total construction costs of $300,000. Estimated completion and occupancy are July 2012.

e. Certain equipment was donated to the corporation by the city. An independent appraisal of the equipment when donated placed the fair value at $16,000 and the residual value at $2,000.

f. Machine A's total cost of $110,000 includes installation charges of $550 and normal repairs and maintenance of $11,000. Residual value is estimated at $5,500. Machine A was sold on February 1, 2011.

g. On October 1, 2010, Machine B was acquired with a down payment of $4,000 and the remaining payments to be made in 10 annual installments of $4,000 each beginning October 1, 2011. The prevailing interest rate was 8%.

Required:

Supply the correct amount for each numbered item on the schedule. Round each answer to the nearest dollar.

Task 2: Depletion; change in estimate

In 2011, the Marion Company purchased land containing a mineral mine for $1,600,000. Additional costs of $600,000 were incurred to develop the mine. Geologists estimated that 400,000 tons of ore would be extracted. After the ore is removed, the land will have a resale value of $100,000.

To aid in the extraction, Marion built various structures and small storage buildings on the site at a cost of $150,000. These structures have a useful life of 10 years. The structures cannot be moved after the ore has been removed and will be left at the site. In addition, new equipment costing $80,000 was purchased and installed at the site. Marion does not plan to move the equipment to another site, but estimates that it can be sold at auction for $4,000 after the mining project is completed.

In 2011, 50,000 tons of ore were extracted and sold. In 2012, the estimate of total tons of ore in the mine was revised from 400,000 to 487,500. During 2012, 80,000 tons were extracted, of which 60,000 tons were sold.

Required:

1. Compute depletion and depreciation of the mine and the mining facilities and equipment for 2011 and 2012. Marion uses the units-of-production method to determine depreciation on mining facilities and equipment.

2. Compute the book value of the mineral mine, structures, and equipment as of December 31, 2012.

3. Discuss the accounting treatment of the depletion and depreciation on the mine and mining facilities and equipment.