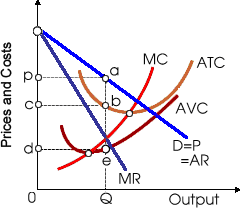

Total cost for that monopolistic competitor in shown below figure equals area: (w) 0cbQ. (x) 0deQ + dcbe. (y) 0paQ cpab. (z) All of the above.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.