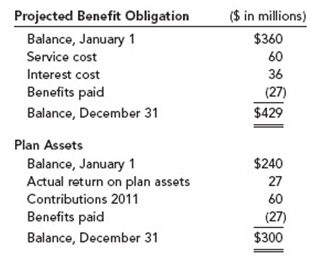

Problem 1: Smith Construction has a noncontributory, defined benefit pension plan. At December 31, 2011, Smith received the following information:

The expected long-term rate of return on plan assets was 10%. There were no AOCI balances related to pensions on January 1, 2011. At the end of 2011, Smith amended the pension formula creating a prior service cost of $12 million, one-third of which is related to employees whose pension benefits have vested.

Determine Smith’s pension expense for 2011.

Question 2: On November 30, the Board of Directors of Johnson Corporation amended its pension plan giving retroactive benefits to its employees. The information below is provided at November 30.

Accumulated benefit obligation (ABO) $825,000

Projected benefit obligation (PBO) 900,000

Plain assets (fair value) 307,500

Market-related asset value 301,150

Prior service cost 190,000

Average remaining service life of

employees 10 years

Useful life of pension goodwill 20 years

Using the straight-line method of amortization, the amount of prior service cost charged to expense during the year ended November 30 is (one of the following)

a. $9,500

b. $19,000

c. $30,250

d. $190,000

Question 3:

Bargain Industries adopted a defined benefit pension plan on April 12, 2011. The provisions of the plan were not made retroactive to prior years. A local bank, engaged as trustee for the plan assets, expects plan assets to earn a 10% rate of return. A consulting firm, engaged as actuary, recommends 6% as the appropriate discount rate. The service cost is $150,000 for 2011 and $200,000 for 2012. Year-end funding is $160,000 for 2011 and $170,000 for 2012. No assumptions or estimates were revised during 2011.

Calculate each of the following amounts as of both December 31, 2011, and December 31, 2012:

1. Projected benefit obligation

2. Plan assets

3. Pension expense.

4. Net pension asset or net pension liability