I. Binary Choice Questions:

1. At her current consumption level, Katherine would get half as much marginal utility from an additional bagel than from an additional muffin. If Katherine is maximizing utility, the price of a bagel is

a. Half the price of a muffin

b. Double the price of a muffin

2. A demand curve with unit price elasticity must be a straight line.

a. True

b. False

3. The price elasticity of demand for steak is generally higher than the price elasticity for meat.

a. True

b. False

4. A certain bakery in Madison makes unique, delicious bagels, and its dedicated customers will not adjust their demand in response to a price change. If the owner wants to increase the bakery’s total revenue, she should

a. Raise the price of bagels.

b. Lower the price of bagels.

5. For Plato, Consumption Bundle A (1 cup of caramel macchiato, 20 cups of espresso) and Consumption Bundle B (2 cups of caramel macchiato, 1 cup of espresso) lie on the same indifference curve. From this information, one could infer that

a. Plato enjoys espresso more than caramel macchiato.

b. Plato enjoys caramel macchiato more than espresso.

6. Suppose coffee and donuts are perfect complements for Tim. Considering only Tim’s fixed budget for coffee and donuts, if the price of donuts increases, then

a. The substitution effect between the two goods is 0, and any change in demand for donuts is completely due to the income effect.

b. The income effect between the two goods is 0, and any change in demand for donuts is completely due to the substitution effect.

7. Conditions that are necessary for a market to be perfectly competitive include:

a. All firms face an inelastic demand for their product.

b. Firms can easily buy and sell the productive resources necessary to compete in the market.

8. In the long run, all firms in a competitive market are indifferent between producing the long run equilibrium level of output and shutting down since at the long-run equilibrium, both accounting profits and fix costs for the firms are equal to zero.

a. True

b. False

9. In the long run, in a perfectly competitive market, the price of a good is determined primarily by the

a. Per-unit cost of production.

b. Decisions of buyers about how much they are willing to pay for the good.

Use the following information to answer the next question.

Year CPI (BY= 1960) CPI (BY = 1980)

1980 200

2000 300 A

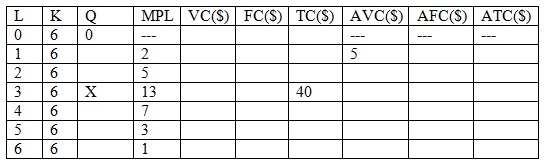

2009 400 B

10. Solve for A and B, respectively.

a. 150; 200

b. 200; 300

11. When the price of good X decreases by 10%, the quantity demanded of good X increases by 20% and the quantity of a complement, good Y, increases by 30%. Calculate the cross-price elasticity of demand for good Y, with respect to the price of good X. (Warning: some information given in this problem is not used for the calculation.)

a. - 2

b. - 3

12. Which of the following statements is true whether the time period is the short run or the long run? The level of output chosen by profit maximizing firms is where

a. Average total costs are minimized.

b. Marginal revenue equals marginal cost.

13. A firm is producing at an output level such that the firm’s average variable cost is greater than its marginal cost. If this firm produces one additional unit of output, how will its average variable cost change?

a. The firm’s average variable cost will increase.

b. The firm’s average variable cost will decrease.

II Multiple Choice Questions:

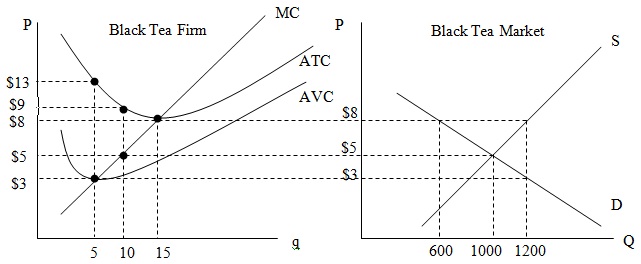

Use the following information and graph to answer the next four (4) questions.

The two graphs below represent the initial equilibrium in the perfectly competitive industry for black tea.

14. What is the profit-maximizing quantity of output that this firm will choose to produce in the short run?

a. 0 units of output

b. 5 units of output

c. 10 units of output

d. 15 units of output

15. At the profit-maximizing point of production in the short run, the firm’s total costs are

a. $0, since the firm will not choose to produce at the given market price.

b. $120.

c. $50.

d. $90.

16. What is the value of fixed cost for this firm?

a. $0.

b. $40.

c. $50.

d. There is not enough information to provide an answer.

17. In the long run, how many firms will there be in this market? Assume that neither the firm’s ATC curve nor the market demand curve changes.

a. 80 firms

b. 40 firms

c. 100 firms

d. 0 firms

18. Pepsi One is a close substitute for Diet Coke. When Pepsi introduced Pepsi One, which of the following most likely happened?

a. The supply for Diet Coke shifted left and became more inelastic.

b. The supply for Diet Coke shifted right and became more inelastic.

c. The demand for Diet Coke shifted left and became more elastic.

d. The demand for Diet Coke shifted right and became more elastic.

Use the following information to answer the next two (2) questions.

Suppose the CPI for the country of Timberland in 2009 is measured as 300, using 2008 as the base year and a scale factor of 100. Tom is a guitarist in one of Timberland’s most famous rock bands. The price of a Gibson guitar in 2009 is $1,200 in Timberland currency, while the price in 2008 was $600.

19. Tom received a coupon from Gibson Company worth $2,400 in Timberland currency. He received the coupon at the beginning of 2008, but he hasn’t used it yet. It is set to expire at the end of 2009. What is the difference in the amount of guitars Tom could have bought using the coupon in 2008 versus using it now in 2009?

a. 0

b. 1

c. 2

d. 3

20. What is the difference in the real price level of a Gibson guitar between 2008 and 2009 in constant 2008 Timberland currency?

a. Gibson guitars are $200 more expensive in real terms in 2009 relative to 2008.

b. Gibson guitars are $200 cheaper in real terms in 2009 relative to 2008.

c. Gibson guitars are $120 more expensive in real terms in 2009 relative to 2008.

d. Gibson guitars are $120 cheaper in real terms in 2009 relative to 2008.

21. Arthur Dent earns $65 every week, all of which he spends on coffee and savory scones. He buys 5 cups of coffee and 15 savory scones. After buying these goods, his marginal utility of buying another cup of coffee is 12 and his marginal utility of buying another savory scone is 3. Each cup of coffee costs $4 and each savory scone costs $3. Then which of the following statements is true?

a. The consumption plan depicted above is not affordable.

b. He is spending his income on coffee and savory scones in such a way as to maximize his utility.

c. He is not maximizing his utility. He should consume more savory scones and less coffee.

d. He is not maximizing his utility. He should consume more coffee and fewer savory scones.

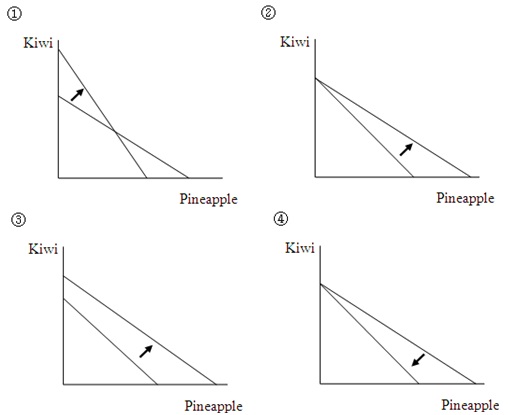

22. Jenny spends all of her income on two fruits: kiwis and pineapples. Suppose the price of pineapples increases, and Jenny’s income increases, while the price of kiwis is unchanged. Which of the following graphs most accurately expresses the change in her budget line?

a. Graph 1

b. Graph 2

c. Graph 3

d. Graph 4

23. Suppose the hand weight market in the U.S. is perfectly competitive in long run equilibrium. Currently, the price of 5-pound hand weights is $20, and all 100 firms in the market are producing at the profit-maximizing quantity of 1000 units. Thus, we can say that marginal cost for each firm is

a. $5.

b. $50.

c. $500.

d. $20.

Use the following information to answer the next two (2) questions.

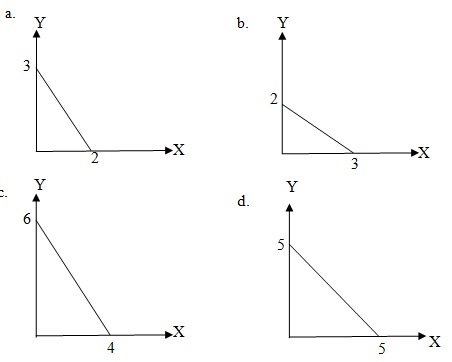

Jack loves Yoplait. He receives 4 units of utility from each Strawberry Yoplait, and 6 units of utility from each Blackberry Yoplait. They are perfect substitutes for Jack.

24. The following graphs measure consumption of Strawberry Yoplait on the x-axis and Blackberry Yoplait on the y-axis. Which of the following indifference curves represents 12 units of utility to Jack from consumption of Strawberry and Blackberry Yoplait?

25. Jack has a budget of $10 with which to buy Yoplait. Each cup of yogurt costs $2, regardless of flavor. How many cups of each flavor should Jack consume to maximize his utility?

a. 5 strawberry, 0 blackberry

b. 0 strawberry, 5 blackberry

c. 4 strawberry, 3 blackberry

d. Every combination satisfying his budget constraint will maximize his utility.

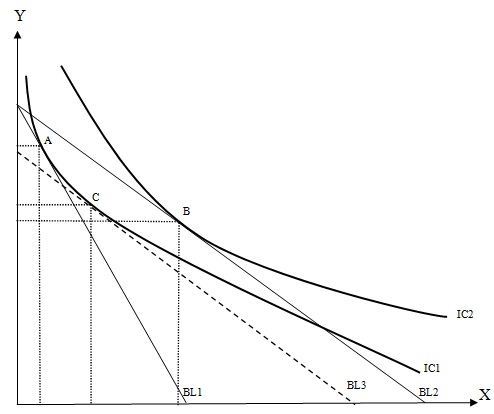

Use the following graph to answer the next two (2) questions.

26. This graph summarizes consumption possibilities over two goods, Good X and Good Y. Budget Line 1 (BL1) depicts a budget constraint with PX=$20, PY=$10, Income=$100. Point A is the optimal consumption choice under the budget constraint expressed by BL1. The marginal rate of substitution of Good X for Good Y at Point A must be

a. 10.

b. 2.

c. 20.

d. There is not enough information given in the problem to answer this question.

27. Hugh recognized that this graph could be used to analyze income and substitution effects of a price change. He made the following conclusions after interpreting this graph, but only one of his conclusions is true. Which of the following conclusions is true?

a. The price of Good X increases in a move from BL1 and BL2.

b. Good X is relatively cheaper given budget line BL3 as compared to budget line BL1, so the consumer prefers Point C to Point A.

c. Good X is a normal good.

d. Good Y is a normal good.

Use the following information to answer the next two (2) questions.

Firm HH produces bicycles. The table below is firm HH’s short run Total Cost Table.

Quantity Total Cost

0 21

2 50

6 140

7 161

10 280

28. What is the average variable cost of producing 7 bicycles? Round your answer to the nearest whole dollar amount.

a. $18/bicycle

b. $20/bicycle

c. $23/bicycle

d. $25/bicycle

29. Due to a new rental agreement, HH’s fixed costs have increased by $10. After this change in fixed costs, what is the marginal cost of one additional bicycle, when the firm is producing 6 bicycles? Round to the nearest whole dollar amount.

a. $21/bicycle

b. $31/bicycle

c. $41/bicycle

d. $51/bicycle

30. Economic costs are ________ accounting costs. Economic profits are ________ accounting profits.

a. At least as great as; no greater than

b. At least as great as; at least as great as

c. No greater than; no greater than

d. No greater than; at least as great as

31. Ryan decides to quit his $40,000 a year job to start his own company. In order to pay for the initial investment, Ryan spends his savings of $10,000 which otherwise would result in an interest payment of 5% each year to Ryan. In its first year, Ryan’s company generates sales revenue of $50,000 and its total operating expenses are $10,000. Given this information, what is Ryan’s economic profit for the first year?

a. -$500

b. $0

c. $40,000

d. $50,000

Use the following information and graph to answer the next three (3) questions.

The following table gives cost information for a firm. Assume that labor is paid a constant wage, i.e. our firm is a price-taker in the labor market. Also, assume that the price of capital is constant.

32. According to the information in the table,

a. X= 5 units of output

b. X= 10 units of output

c. X= 15 units of output

d. X= 20 units of output

33. According to the information in the table, what is the fixed cost of this firm?

a. $5

b. $10

c. $15

d. $20

34. According to the information in the table, what is the wage rate (that is, what is the price of a unit of labor)?

a. $5 per unit of labor

b. $10 per unit of labor

c. $15 per unit of labor

d. $20 per unit of labor

35. Firm A produces in a market with many firms and therefore Firm A cannot influence the market price. Currently Firm A is producing at an output level where its average total cost is equal to the market price. At this level of production, Firm A’s average total cost is greater than its marginal cost. Assume that there is no change in the market price of the good. If Firm A wants to maximize its profits, Firm A should

a. Shut down immediately.

b. Produce less in the short run and shut down in the long run.

c. Produce more in the short run and continue to operate in the long run.

d. Produce at the current production level in the short run and in the long run.

36. Increasing Returns to Scale (IRTS) refers to

a. The situation in the long run where the firm’s average total cost decreases as the size of the plant increases.

b. The situation in the long run where the firm’s average total cost increases as the size of the plant increases.

c. The situation in the short run where the average total cost decreases when the quantity of input factors is increased by some amount.

d. The situation in the short run where the average total cost increases when the quantity of input factors is increased by some amount.

37. The short run total cost function of a representative firm in a perfectly competitive market is given by the equation TC = q2 + 100q + 100, where q denotes the units of output produced by the firm. The implied short run marginal cost curve for a representative firm is therefore MC = 2q + 100. Assume the market demand is given by P = 300 – Q where the market quantity demanded is Q. Suppose the short run equilibrium price of output is $120. How many firms are in this industry in the short run?

a. 10 firms

b. 12 firms

c. 18 firms

d. 180 firms