Assignment:

Question 1 Competitive markets are characterized by

a) a small number of buyers and sellers.

b) unique products.

c) the interdependence of firms

d) free entry and exit by firms.

Question 2 Suppose that a firm in a competitive market is currently maximizing its short-run profit at an output of 50 units. If the current price is $9, the marginal cost of the 50th unit is $9, and the average total cost of producing 50 units is $4, what is the firm's profit?

a) $0

b) $200

c) $250

d) $450

Question 3 The accountants hired by the Brookside Racquet Club have determined total fixed cost to be $75,000, total variable cost to be $130,000, and total revenue to be $145,000. Because of this information, in the short run, the Brookside Racquet Club should

a) shut down.

b) exit the industry.

c) stay open because shutting down would be more expensive.

d) stay open because the firm is making an economic profit.

Question 4 Suppose that a firm in a competitive market faces the following revenues and costs:

|

Quantity

|

Total Revenue

|

Total Cost

|

|

0

|

$0

|

$10

|

|

1

|

$9

|

$14

|

|

2

|

$18

|

$19

|

|

3

|

$27

|

$25

|

|

4

|

$36

|

$32

|

|

5

|

$45

|

$40

|

|

6

|

$54

|

$49

|

|

7

|

$63

|

$59

|

|

8

|

$72

|

$70

|

|

9

|

$81

|

$82

|

Refer to Table above. If the firm's marginal cost is $11, it should

a) increase production to maximize profit.

b) increase the price of the product to maximize profit.

c) advertise to attract additional buyers to maximize profit.

d) reduce production to increase profit.

Question 5 If a competitive firm is currently producing a level of output at which marginal revenue exceeds marginal cost, then

a) a one-unit increase in output will increase the firm's profit.

b) a one-unit decrease in output will increase the firm's profit.

c) total revenue exceeds total cost.

d) total revenue exceeds total cost.

Question 6 For a firm in a competitive market, an increase in the quantity produced by the firm will result in

a) a decrease in the product's market price.

b) an increase in the product's market price.

c) no change in the product's market price.

d) either an increase or no change in the product's market price depending on the number of firms in the market.

Question 7 Which of the following industries is most likely to exhibit the characteristic of free entry?

a) nuclear power

b) municipal water and sewer

c) dairy farming

d) airport security

Question 8 Competitive firms that earn a loss in the short run should

a) shut down if P < AVC.

b) raise their price.

c) lower their output.

d) All of the above are correct.

Question 9 Which of the following statements best expresses a firm's profit-maximizing decision rule?

a) If marginal revenue is greater than marginal cost, the firm should increase its output.

b) If marginal revenue is less than marginal cost, the firm should decrease its output.

c) If marginal revenue equals marginal cost, the firm should continue producing its current level of output.

d) All of the above are correct.

Question 10 Refer to Table above. For a firm operating in a competitive market, the marginal revenue

|

Quantity

|

Total Revenue

|

|

0

|

$0

|

|

1

|

$7

|

|

2

|

$14

|

|

3

|

$21

|

|

4

|

$28

|

a) $0.

b) $7.

c) $14.

d) $21.

Question 11 Comparing marginal revenue to marginal cost

(i) reveals the contribution of the last unit of production to total profit.

(ii) is helpful in making profit-maximizing production decisions.

(iii) tells a firm whether its fixed costs are too high.

a) (i) only

b) (i) and (ii) only

c) (ii) and (iii) only

d) (i) and (iii) only

Question 12 Suppose a firm in a competitive market produces and sells 150 units of output and earns $1,800 in total revenue from the sales. If the firm increases its output to 200 units, the average revenue of the 200th unit will be

a) less than $12.

b) more than $12.

c) $12.

d) Any of the above may be correct depending on the price elasticity of demand for the product.

Question 13 Which of the following statements best reflects a price-taking firm?

a) If the firm were to charge more than the going price, it would sell none of its goods.

b) The firm has an incentive to charge less than the market price to earn higher revenue.

c) The firm can sell only a limited amount of output at the market price before the market price will fall.

d) Price-taking firms maximize profits by charging a price above marginal cost.

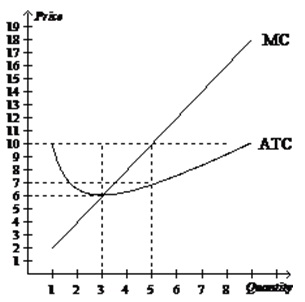

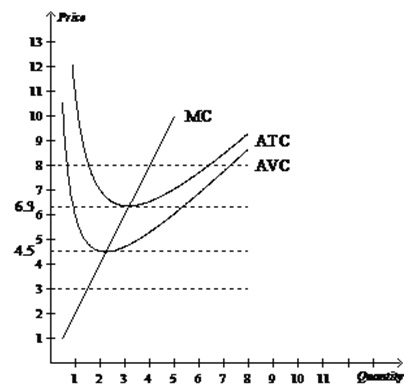

Question 14 Suppose a firm operating in a competitive market has the following cost curves:

Refer to Figure above . If the market price is $10, what is the firm's total revenue?

a) $15

b) $30

c) $35

d) $50

Question 15 Consider a firm operating in a competitive market. The firm is producing 40 units of output, has an average total cost of production equal to $5, and is earning $240 economic profit in the short run. What is the current market price?

a) $9

b) $10

c) $11

d) $12

Question 16 Cold Duck Airlines flies between Tacoma and Portland. The company leases planes on a year-long contract at a cost that averages $600 per flight. Other costs (fuel, flight attendants, etc.) amount to $550 per flight. Currently, Cold Duck's revenues are $1,000 per flight. All prices and costs are expected to continue at their present levels. If it wants to maximize profit, Cold Duck Airlines should

a) drop the flight immediately.

b) continue the flight.

c) continue flying until the lease expires and then drop the run.

d) drop the flight now but renew the lease if conditions improve.

Question 17 Which of the following firms is the closest to being a perfectly competitive firm?

a) the New York Yankees

b) Apple, Inc.

c) DeBeers diamond wholesalers

d) a wheat farmer in Kansas

Question 18 Mrs. Smith operates a business in a competitive market. The current market price is $8.50. At her profit-maximizing level of production, the average variable cost is $8.00, and the average total cost is $8.25. Mrs. Smith should

a) shut down her business in the short run but continue to operate in the long run.

b) continue to operate in the short run but shut down in the long run.

c) continue to operate in both the short run and long run.

d) shut down in both the short run and long run.

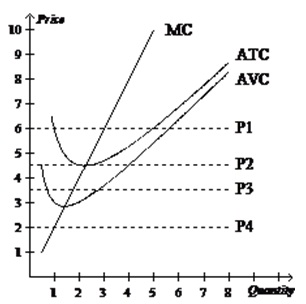

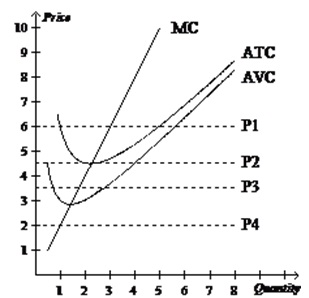

Question 19 Suppose a firm operating in a competitive market has the following cost curves:

Refer to Figure above. Which of the four prices corresponds to a firm earning positive economic profits in the short run?

a) P1

b) P2

c) P3

d) P4

Question 20 Suppose that a firm in a competitive market faces the following revenues and costs:

|

Quantity

|

Total Revenue

|

Total Cost

|

|

0

|

$0

|

$3

|

|

1

|

$7

|

$5

|

|

2

|

$14

|

$9

|

|

3

|

$21

|

$15

|

|

4

|

$28

|

$23

|

|

5

|

$35

|

$33

|

|

6

|

$42

|

$45

|

|

7

|

$49

|

$59

|

Refer to Table above. Which level of production in the table has the lowest average variable cost?

a) 1 unit

b) 2 units

c) 3 units

d) 4 units

Question 21 Whenever a perfectly competitive firm chooses to change its level of output, its marginal revenue

a) increases if MR < ATC and decreases if MR > ATC.

b) does not change.

c) increases.

d) decreases.

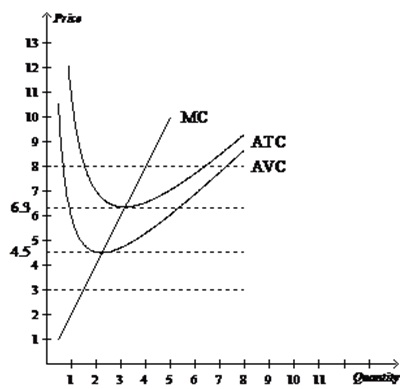

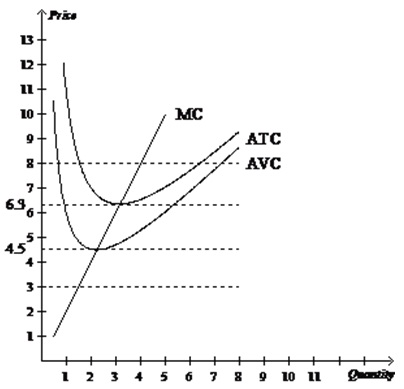

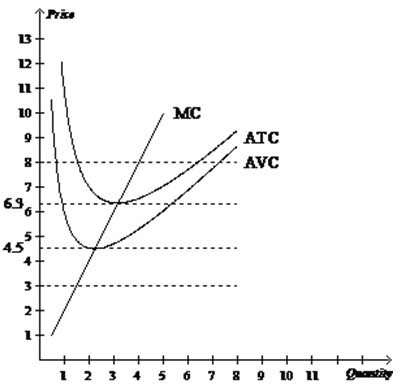

Question 22 Suppose that a firm in a competitive market has the following cost curves:

Refer to Figure above. If the market price is $6.30, the firm will earn

a) positive economic profits in the short run.

b) negative economic profits in the short run but remain in business.

c) negative economic profits and shut down.

d) zero economic profits in the short run.

Question 23 Profit-maximizing firms enter a competitive market when existing firms in that market have

a) total revenues that exceed fixed costs.

b) total revenues that exceed total variable costs.

c) average total costs that exceed average revenue.

d) average total costs less than market price.

Question 24 Suppose that a firm in a competitive market has the following cost curves:

Refer to Figure above. If the market price is $6.30, the firm will earn

a) positive economic profits in the short run.

b) negative economic profits in the short run but remain in business.

c) negative economic profits and shut down.

d) zero economic profits in the short run.

Question 25 Suppose a firm in each of the two markets listed below were to increase its price by 30 percent. In which pair would the firm in the first market listed experience a dramatic decline in sales, but the firm in the second mar-ket listed would not?

a) oil and natural gas

b) cable television and gasoline

c) restaurants and MP3 players

d) movie theaters and ballpoint pens

Question 26 If a firm in a perfectly competitive market triples the quantity of output sold, then total revenue will

a) more than triple.

b) less than triple.

c) exactly triple.

d) Any of the above may be true depending on the firm's labor productivity.

Question 27 When firms are said to be price takers, it implies that if a firm raises its price,

a) buyers will go elsewhere.

b) buyers will pay the higher price in the short run.

c) competitors will also raise their prices.

d) firms in the industry will exercise market power.

Question 28 Suppose that a firm in a competitive market has the following cost curves:

Refer to Figure above. If the market price falls below $4.50, the firm will earn

a) positive economic profits in the short run.

b) negative economic profits in the short run but remain in business.

c) negative economic profits in the short run and shut down.

d) zero economic profits in the short run.

Question 29 Suppose that a firm in a competitive market has the following cost curves:

Refer to Figure above. The firm should shut down if the market price is

a) above $8.

b) above $6.30 but less than $8.

c) above $4.50 but less than $6.30.

d) less than $4.50.

Question 30 When a profit-maximizing firm is earning profits, those profits can be identified by

a) P x Q.

b) (MC - AVC) x Q.

c) (P - ATC) x Q.

d) (P - AVC) x Q.

Question 31 Suppose that a firm in a competitive market faces the following revenues and costs:

|

Quantity

|

Total Revenue

|

Total Cost

|

|

0

|

$0

|

$10

|

|

1

|

$9

|

$14

|

|

2

|

$18

|

$19

|

|

3

|

$27

|

$25

|

|

4

|

$36

|

$32

|

|

5

|

$45

|

$40

|

|

6

|

$54

|

$49

|

|

7

|

$63

|

$59

|

|

8

|

$72

|

$70

|

|

9

|

$81

|

$82

|

Refer to Table above. In order to maximize profit, the firm will produce a level of output where marginal reve-nue is equal to

a) $6.

b) $7.

c) $8.

d) $9.

Question 32 Refer to Table above. For a firm operating in a competitive market, the average revenue is

a) $45.

b) $30.

c) $15.

d) $0.

Question 33 Suppose a firm operating in a competitive market has the following cost curves:

Refer to Figure above. Which of the four prices corresponds to a firm earning negative economic profits in the short run but trying to remain open?

a) P1

b) P2

c) P3

d) P4

Question 34 Suppose that a firm in a competitive market has the following cost curves:

Refer to Figure above. If the market price rises above $6.30, the firm will earn

a) positive economic profits in the short run.

b) negative economic profits in the short run but remain in business.

c) negative economic profits and shut down.

d) zero economic profits in the short run.

Question 35 Suppose you value a special watch at $100. You purchase it for $75. On your way home from class one day, you lose the watch. The store is still selling the same watch, but the price has risen to $85. Assume that losing the watch has not altered how you value it. What should you do?

a) Pay the $85 to buy the watch.

b) Wait to see if the watch goes on sale. If the price drops to $75 or less, buy the watch.

c) Wait to see if the watch goes on sale. If the price drops to $25 or less, buy the watch.

d) Do not buy the watch.

Question 36 Suppose a certain competitive firm is producing Q=500 units of output. The marginal cost of the 500th unit is $17, and the average total cost of producing 500 units is $12. The firm sells its output for $20.

Refer to Scenario . At Q=499, the firm's total costs equal

a) $5,983.

b) $5,988.

c) $5,995.

d) $5,999.

Question 37 Diana's Dress Emporium

|

COSTS

|

REVENUES

|

|

Quantity

Produced

|

Total

Cost

|

Marginal

Cost

|

Quantity

Demanded

|

Price

|

Total

Revenue

|

Marginal

Revenue

|

|

0

|

$100

|

--

|

0

|

$120

|

|

--

|

|

1

|

$150

|

|

1

|

$120

|

|

|

|

2

|

$202

|

|

2

|

$120

|

|

|

|

3

|

$257

|

|

3

|

$120

|

|

|

|

4

|

$317

|

|

4

|

$120

|

|

|

|

5

|

$385

|

|

5

|

$120

|

|

|

|

6

|

$465

|

|

6

|

$120

|

|

|

|

7

|

$562

|

|

7

|

$120

|

|

|

|

8

|

$682

|

|

8

|

$120

|

|

|

Refer to Table above. What is the marginal cost of the 1st unit?

a) $50

b) $75

c) $80

d) $150

Question 38 When a restaurant stays open for lunch service even though few customers patronize the restaurant for lunch, which of the following principles is (are) best demonstrated?

(i) Fixed costs are sunk in the short run.

(ii) In the short run, only fixed costs are important to the decision to stay open for lunch.

(iii) If revenue exceeds variable cost, the restaurant owner is making a smart decision to remain open for lunch.

a) (i) and (ii) only

b) (ii) and (iii) only

c) (i) and (iii) only

d) (i), (ii), and (iii)

Question 39 Suppose that a firm in a competitive market faces the following prices and costs:

|

Price

|

Quantity

|

Total

Cost

|

|

$5

|

0

|

$3

|

|

$5

|

1

|

$5

|

|

$5

|

2

|

$8

|

|

$5

|

3

|

$12

|

|

$5

|

4

|

$17

|

|

$5

|

5

|

$23

|

Refer to Table above. The marginal revenue from producing the 3rd unit equals

(i) $5.

(ii) the price.

(iii) the marginal cost.

a) (i) only

b) (i) and (ii) only

c) (ii) only

d) (i), (ii), and (iii)

Question 40 In a competitive market, no single producer can influence the market price because

a) many other sellers are offering a product that is essentially identical.

b) consumers have more influence over the market price than producers do.

c) government intervention prevents firms from influencing price.

d) producers agree not to change the price.

Question 41 The firm will make the most profits if it produces the quantity of output at which

a) marginal cost equals average cost.

b) profit per unit is greatest.

c) marginal revenue equals total revenue.

d) marginal revenue equals marginal cost

Question 42 Suppose that a firm in a competitive market faces the following revenues and costs:

|

Quantity

|

Total Revenue

|

Total Cost

|

|

0

|

$0

|

$10

|

|

1

|

$9

|

$14

|

|

2

|

$18

|

$19

|

|

3

|

$27

|

$25

|

|

4

|

$36

|

$32

|

|

5

|

$45

|

$40

|

|

6

|

$54

|

$49

|

|

7

|

$63

|

$59

|

|

8

|

$72

|

$70

|

|

9

|

$81

|

$82

|

Refer to Table above At which quantity of output is marginal revenue equal to marginal cost?

a) 3 units

b) 6 units

c) 8 units

d) 9 units

Question 43 A firm that has little ability to influence market prices operates in a

a) competitive market.

b) strategic market.

c) thin market.

d) power market.

Question 44 Suppose that a firm in a competitive market faces the following revenues and costs:

|

Quantity

|

Total Revenue

|

Total Cost

|

|

0

|

$0

|

$3

|

|

1

|

$7

|

$5

|

|

2

|

$14

|

$9

|

|

3

|

$21

|

$15

|

|

4

|

$28

|

$23

|

|

5

|

$35

|

$33

|

|

6

|

$42

|

$45

|

|

7

|

$49

|

$59

|

Refer to Table above. If the firm produces the profit-maximizing level of production, how much profit will the firm earn?

a) $2

b) $4

c) $6

d) $8

Question 45 In the long run, a firm will exit a competitive industry if

a) total revenue exceeds total cost.

b) the price exceeds average total cost.

c) average total cost exceeds the price.

d) Both a and b are correct.