Assume the bakery in Question 2 is one out of 100 identical firms working in a perfectly competitive industry. Hence each of the100 identical firms will have a cost schedule as calculated in Table 1 in Question1. 1. The market demand schedule for the bread product sold by this industry is given in Table 2.

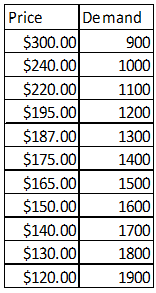

Table 2

(a) Using the information provided, derive the supply schedule for an individual firm, and the industry supply schedule. (Note: You need to use a standard computer package to derive your answers). The relevant output(s) should form part of the main report and substantive evidence of how you obtained the answers should be included in the Appendix).

(b) Determine the equilibrium market price and the equilibrium market output level.

(c) Determine the individual's firm's level of profit. Profit = TR - TC

(d) Discuss why the equilibrium point that you have determined in part (b) is deemed a short run equilibrium point.

(e) Is this point going to be the same in the long run? If not, discuss what the long run equilibrium would be?