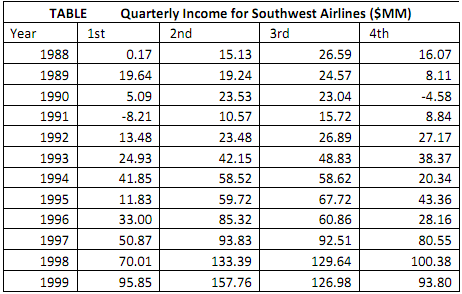

Problem 1. Table contains Southwest Airlines' quarterly income before extraordinary items ($MM) for the years 1988-1999.

a. Plot the income data as a time series and describe any patterns that exist.

b. Is this series stationary or nonstationary? Explain.

c. Using Excel, compute the autocorrelations of the income series for the first 10 time lags. Is the behavior of the autocorrelations consistent with your choice in part b? Explain.

Problem 2.

a. Consider a naive forecasting method where the first-quarter income is used to forecast first-quarter income for the following year, second-quarter income is used to forecast second-quarter income,and so forth.For example,a forecast of first-quarter income for 1998 is provided by the first-quarter income for 1997, 50.87 (see Table P-23).Use this naive method to calculate forecasts of quarterly income for the years 1998-1999.

b. Using the forecasts in part a,calculate the MAD, RMSE,and MAPE.

c. Given the results in part b and the nature of the patterns in the income series, do you think this naive forecasting method is viable? Can you think of another naive method that might be better?