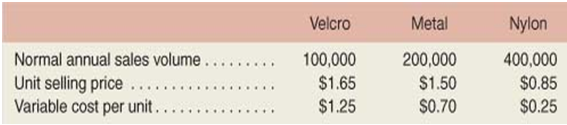

Cheryl Montoya picked up the phone and called her boss, Wes Chan, the vice president of marketing at Piedmont Fasteners Corporation: "Wes, I'm not sure how to go about answering the questions that came up at the meeting with the president yesterday.""What's the problem?""The president wanted to know the break-even point for each of the company's products, but I am having trouble figuring them out.""I'm sure you can handle it, Cheryl. And, by the way, I need your analysis on my desk tomorrow morning at 8:00 sharp in time for the follow-up meeting at 9:00."Piedmont Fasteners Corporation makes three different clothing fasteners in its manufacturing facility in North

Carolina. Data concerning these products appear below:

Total fixed expenses are $400,000 per year.

All three products are sold in highly competitive markets, so the company is unable to raise its prices without losing unacceptable numbers of customers.

The company has an extremely effective lean production system, so there are no beginning or ending work in process or finished goods inventories.

1. Calculate what the company's over-all break-even point in total sales dollars. Explain your methodology (approximately 2 pages).

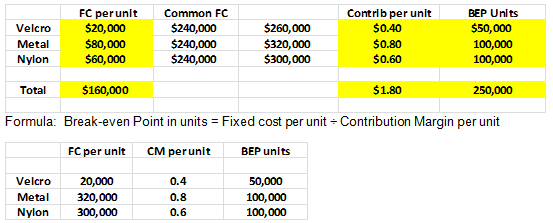

Of the total fixed costs of $400,000, $20,000 could be avoided if the Velcro product were dropped, $80,000 if the Metal product were dropped, and $60,000 if the Nylon product were dropped. The remaining fixed costs of $240,000 consist of common fixed costs such as administrative salaries and rent on the factory building that could be avoided only by going out of business entirely (approximately 2 pages):

2a.Calculate the break-even point in units for each product. Explain your methodology.

b. Explain if the company sells exactly the break-even quantity of each product, what will be the overall profit of the company and show your results.

3. Compare and explain if this company should be using a job order or process-costing system to accumulate costs (one page).

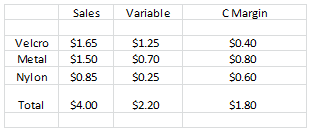

Formula: Sales = units sold * selling price per unit

Velcro - 100,000 * $1.65 = $165,000

Metal - 200,000 * $1.50 = $ 300,000

Nylon - 400,000 * $0.85 = $ 340,000

Total Sales $ 805,000

Formula: Variable Cost per unit * unit sold

Velcro -$1.25 * 100,000 = $ 125,000

Metal - $0.70 * 200,000 = $ 140,000

Nylon - $0.25 * 400,000 = $ 100,000

Total Variable $ 365,000

Formula: Sales- Variable = Contribution Margin

$805,000 - $365,000 = $440,000

|

Piedmont Fasteners Corp.

Projected Annual Net Income

Sales $ 805,000

Variable Expenses - 365,000

Contribution Margin 440,000

Fixed Expenses - 400,000

Net Income $ 40,000

|

Formula: CM ratio = CM= $ 440,000 = 0.54658 = 54.6%

Sales $ 850,000

Break Even Point in total sales dollars = FC/CMR = $400,000/ 54.6% = $732,600.73

Velcro

Sales (50,000units @ $1.65) $82,500

Variable (50,000 units @ $1.25) - 62,500

Contribution Margin 20,000

Less: Fixed Cost for Velcro - 20,000

Profit 0

Metal

Sales (100,000units @ $1.50) $150,000

Variable (100,000units @ $0.70) - 70,000

Contribution Margin 80,000

Less: Fixed Cost for Metal - 80,000

Profit 0

Nylon

Sales (100,000units @ $0.85) $85,000

Variable (100,000units @ $0.25) - 25,000

Contribution Margin 60,000

Less: Fixed Cost for Velcro - 60,000

Profit 0

|

Piedmont Fasteners Corp.

Overall Net Income

Sales (250,000 @ $4.00) $1,000,000

Variable (250,000 @ $2.20) - 550,000

Contribution Margin 450,000

Less: Fixed Cost - 400,000

Profit $ 50,000

|

There are three reasons Piedmont Fasteners should use job-order to accumulate cost. First, job-order costing should be use because the units of product are not identical. There are different products and the amounts are different(Garrison, Noreen, & Brewer, 2010). Second, costs are not accumulated by a department; it is accumulated by individual products(Garrison, Noreen, & Brewer, 2010). Lastly, unit costs are not computed by department they are computed by job on the job cost sheet(Garrison, Noreen, & Brewer, 2010).