Question 1

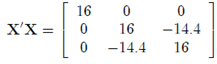

A regression equation with three regressors X1,X2 and X2, is obtained be regressing (yi - y) on (xi1 - x1), (x2 -52) and (2,3 - 23) for t = 1 V where g, 21, 22 and 23 are the sample averages of the regressand y and the three regressors. The observed values of X'X, where

is the (N x 3) matrix of observed deviations from the average, is

Suppose that you estimate the regression model

y = X1β, + X2β2 + X2β3 + e

where e satisfies the classical assumptions and has sample variance s2 = 32. Calculate the variance-covariance matrix of the OLS estimator of β1.β2 and β3 and verify that:

1. The variance of bi is directly proportional to the reciprocal of the observed variance of Xi.

2. The variance of each 62 and 63 is bigger than that of bi even though the observed variance of X2 and X3 is the same as that of Xi. Why is this the case?

3. The covariance between b2 and b3 is positive. Provide a heuristic explanation of this feature.

Attachment:- EM201448JOH328ASTAT_Question.docx