Problem on price level-real domestic output

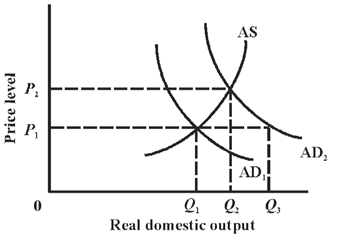

Refer to the below diagram. Give me answer of this question. If equilibrium real output is Q2, then: A) aggregate demand is AD1. B) the equilibrium price level is P1. C) producers will supply output level Q1. D) the equilibrium price level is P2.

Refer to the given diagram. Which of the following positions relative to PP1 would be the most likely to result in a future production possibilities curve of PP3, rather than PP2 ? 1) A. 2) B. 3) C. 4) D. Q : Determine equilibrium by Price Ceilings Between the predictable results while government sets a maximum price below equilibrium are: (1) shortages. (2) queues. (3) black markets and corruption. (4) economic inefficiency. (5) All of the above. Q : How is TVC derived from MC How is TVC How is TVC derived from MC? Answer: TVC = Sigma MC

Between the predictable results while government sets a maximum price below equilibrium are: (1) shortages. (2) queues. (3) black markets and corruption. (4) economic inefficiency. (5) All of the above. Q : How is TVC derived from MC How is TVC How is TVC derived from MC? Answer: TVC = Sigma MC

How is TVC derived from MC? Answer: TVC = Sigma MC

When a firm possesses some market power, in that case the firm’s marginal revenue is negative inside the range of output where demand is: (i) price elastic. (ii) unitarily elastic. (iii) relatively price inelastic. (iv) perfectl

The ratio of the area between the perfect equality reference line and the Lorenz curve is the: (w) Gini index. (x) relative income (y) poverty line (z) marginal productivity standard. Q : Prospective financial investment by Assets turn into less desirable to prospective financial investors while: (w) they become more liquid. (x) interest rates increase. (y) their prices go up. (z) default risks decrease. How can I solve my Eco

Assets turn into less desirable to prospective financial investors while: (w) they become more liquid. (x) interest rates increase. (y) their prices go up. (z) default risks decrease. How can I solve my Eco

I have a problem in economics on Definition of Industry. Please help me in the following question. The industry is stated as: (1) Each and every firm producing all final services and goods. (2) Each and every firm producing the similar product. (3) Th

When cuts into the price of cowboy hats drive down total revenues to hat makers, in that case demand: (1) relatively price elastic. (2) relatively price inelastic. (3) unitarily price elastic. (4) infinitely price elastic. (5) zero pr

When the economy was in a complete equilibrium, in that case the distribution of income would be precisely proportional to the distribution of: (a) taxation. (b) inheritance. (c) luck. (d) wealth.

Price Rigidity: The other significant feature of oligopoly is price rigidity. Price is rigid or sticky at the prevailing level due to the fear of reaction from the rival firms. When an oligo

18,76,764

1924711 Asked

3,689

Active Tutors

1446012

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!