Problem based on shift of the production possibilities curve

Technological advance in producing both capital goods and consumer goods is illustrated by the shift of the production possibilities curve from AB to: 1) CD. 2) EB. 3) AF. 4) GH. Select the right answer for above given question

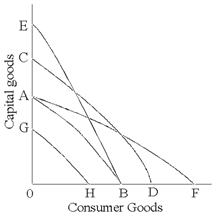

Technological advance in producing both capital goods and consumer goods is illustrated by the shift of the production possibilities curve from AB to: 1) CD. 2) EB. 3) AF. 4) GH.

Select the right answer for above given question

Upon the average, all intermediaries do NOT: (w) decrease the opportunity costs of goods to consumers. (x) raise the incomes of producers. (y) reduce transaction costs. (z) increase the cost of living. Hey friends

Marginal revenue is below average revenue as [TR/Q] for a firm along with market power since: (w) the demand curve this faces is negatively sloped. (x) its supply curve is relatively inelastic. (y) marginal cost is be

The supply curve which would best reflect the supply of 1940 a Packard 180 limousine is as: (i) supply curve S1. (ii) supply curve S2. (iii) supply curve S3. (iv) supply curve S4. (v) supply curve S5.

The social value of additional output from the additional units of labor is as: (1) Marginal revenue product [or MRP] of labor. (2) Wage rate or price of the labor. (3) Average revenue product [or ARP] of labor. (4) Value of marginal product [or VMP] of labor. (5) Mar

Graduate Level Problem Set. First question is in relation to the article the Population Problem: Theory and Evidence by Partha Dasgupta.

When boosting output by hundred units raises total revenue by $1200, in that case a purely competitive firm’s marginal revenue the same as: (w) $1,200. (x) $120. (y) $12. (z) $120,000. I need a good answer on

In this demonstrated figure, the total revenue: (w) varies inversely along with price in range b. (x) is minimized at the midpoint of the demand curve. (y) remains unchanged like price changes within range b. (z) will raise as price falls within range

Refer to the given diagram. Which of the following positions relative to PP1 would be the most likely to result in a future production possibilities curve of PP3, rather than PP2 ? 1) A. 2) B. 3) C. 4) D. Q : Decrease transportation and transaction The value of land is attributable to the ways exactly sites decrease transportation and other transaction costs are termed as: (1) location rents. (2) transportation rents. (3) short term quasi rents. (4) parcel posts. (5) transaction

The value of land is attributable to the ways exactly sites decrease transportation and other transaction costs are termed as: (1) location rents. (2) transportation rents. (3) short term quasi rents. (4) parcel posts. (5) transaction

When Wilma can make a brontosaurus burger in 10 min and a cactus cooler in 5, whereas Betty can make the burger in 8 min and the cactus cooler in 3. Then find out the right option from the above: (1) Betty consists of a comparative disadvantage in the coolers and a co

18,76,764

1946839 Asked

3,689

Active Tutors

1425393

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!