Market initially at price and quantity

This market for peanuts is primarily into equilibrium at price: (w) P0 and quantity Q0 (x) P1 and quantity Q0 (y) P2 and quantity Q2 (z) P1 and quantity Q1 How can I solve my economics problem? Please suggest me the correct answer.

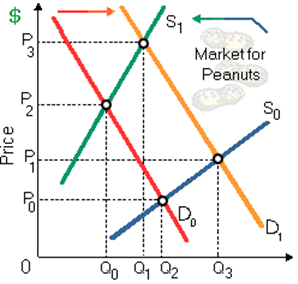

This market for peanuts is primarily into equilibrium at price: (w) P0 and quantity Q0 (x) P1 and quantity Q0 (y) P2 and quantity Q2 (z) P1 and quantity Q1

How can I solve my economics problem? Please suggest me the correct answer.

Describe the steps taken in estimating N.I. by product/ value added technique? Answer: A) Classify all production units: Locate

Describe how changes in the prices of other products influence the supply of a specific product.

The marginal utility curve can much loosely be translated into the demand curve by: (1) Measuring its declining part in dollars. (2) Transforming utils into the prices. (3) Horizontally summing up everyone’s MUs at each and every price. (4) Setting MUa/Pa = MUb/

Most of the economists believe firms tend to proficiently maximize the profits since of: (i) Stockholder pressure. (ii) Competition for the management positions. (iii) Principal-agent conditions. (iv) The chance of corporate take-over. Q : Short-run consequence of hurricanes A probable short-run consequence of a devastating sequence of hurricanes smashing by Florida would be: (w) reductions within the prices of building materials. (x) raises the price of tickets at Disney World. (y) declining demand for Florida oranges due to higher price

A probable short-run consequence of a devastating sequence of hurricanes smashing by Florida would be: (w) reductions within the prices of building materials. (x) raises the price of tickets at Disney World. (y) declining demand for Florida oranges due to higher price

Can someone help me in finding out the right answer from the given options. In the marginality, profit-maximizing model of firm, a firm which can’t wage discriminate maximizes profit if labor is hired at a point where: (1) Price = MFC. (2) MRP = VMP. (3) MRP = M

Monopolistic competitors generate levels of output which are: (w) more than socially optimal and equitable. (x) economically efficient. (y) where marginal social benefits exceed marginal social costs. (z) certain to generate economic profits.

Cameron is performing a research project on whale migration at Pacific Ocean. To assist with this research she hires a Ph.D. from the MIT to make computer software to organize data, paying the software genius $150,000 for his services. The Ph.D. assures Cameron that t

The labor union contracts, a comparable worth rule, or minimum salary laws might boost up equilibrium employment when a firm has been practicing: (i) Price discrimination. (ii) Monopolistic exploitation. (iii) Feather-bedding. (iv) Blacklisting. (v) Monopsonistic expl

What supply curve illustrates?

18,76,764

1957842 Asked

3,689

Active Tutors

1421916

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!