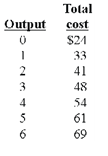

Marginal cost

Give the answer of following question. Refer to the given data. The marginal cost of producing the sixth unit of output is: A) $24. B) $12. C) $16. D) $8.

For a monopolist to raise the quantity of its products sold needs the monopolist to as: (i) raise the price of its product. (ii) charge a constant price. (iii) invest heavily in a distribution network. (iv) lower the price of its product. (v) advertis

The demand curve that facing a monopolistically competitive firm is: (1) perfectly elastic within the short run. (2) perfectly inelastic due to numerous substitutes for its product. (3) less elastic than the demand curve facing a comp

The maximum amounts of a good that people are willing and capable to buy at different market prices during a specific period are depicted by: (1) Horizontal summations. (2) Income or satisfaction boundaries. (3) Demand curves. (4) Consumption possibilities frontiers.<

Whenever an organization’s wage structure reflects the keenness of individual staff to work, terms which are most applicable comprise: (p) Monopsonistic exploitation & wage discrimination. (q) Monopolistic exploitation and the separation of possession and co

The Diamante Corporation is vast and owns the world’s merely red diamond mine. Thus diamante monopolizes the market for red diamonds, and this is protected by competition by a: (1) regulatory barrier to entry. (2) strategic barrier to entry. (3) natural barrier

I have a problem in economics on Influence of Demand in the market price of good. Please help me in the following question. In short run, a demand curve would not shift the following a change in: (i) The size and distribution of national income. (ii)

Welfare is explained as being received while: (w) the ratios of personal benefits received by government programs associate to taxes paid are greater than for the average citizen. (x) economic rents are earned by owners of inputs. (y) a productive inp

The demand curve which is least consistent along with the existence of a substitution consequence is within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Q : Legal barriers to entry in a market Governmentally-imposed obstacles to the entrance of new firms within a market are termed as: (1) regulatory barriers or legal barriers to entry. (2) strategic barriers to entry. (3) natural barriers to entry. (4) tax barriers to entry. (5) revenue blockades.

Governmentally-imposed obstacles to the entrance of new firms within a market are termed as: (1) regulatory barriers or legal barriers to entry. (2) strategic barriers to entry. (3) natural barriers to entry. (4) tax barriers to entry. (5) revenue blockades.

Possible utilization of a ‘felicific calculation’ to recognize punishments for the crimes was derived from: (1) Medieval scholasticism. (2) Say’s Law. (3) Gresham’s Law. (4) Marshall’s Maxim. (5) Jeremy Bentham&r

18,76,764

1940895 Asked

3,689

Active Tutors

1458083

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!