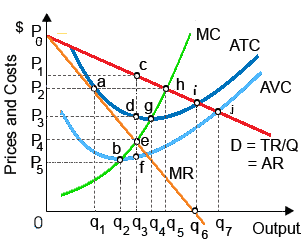

HoloIMAGine has patented a holographic technology which makes 3-D photography obtainable to consumers. When HoloIMAGine is a pure monopoly, in that case this firm confronts a demand curve which is: (w) identical to the industry demand curve. (x) perfectly price inelastic. (y) unitarily price elastic. (z) perfectly price elastic.

Hello guys I want your advice. Please recommend some views for above Economics problems.