Determine short-run supply of an industry

The Christmas tree industry’s short-run supply is demonstrated as: (1) curve A. (2) curve B. (3) curve E. (4) curve F. (5) curve G. Hello guys I want your advice. Please recommend some views for above Economics problems.

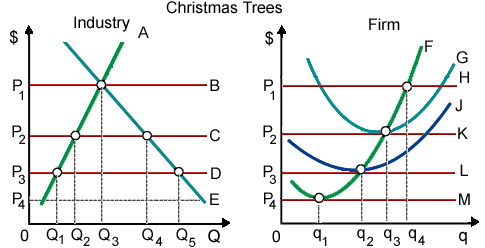

The Christmas tree industry’s short-run supply is demonstrated as: (1) curve A. (2) curve B. (3) curve E. (4) curve F. (5) curve G.

Hello guys I want your advice. Please recommend some views for above Economics problems.

The bilateral monopoly is in operation when: (i) Firm is the only employer of the certain labor force and a union is just the supplier of the labor for that organization. (ii) The firm is the mere producer of the two complementary goods. (iii) The monopolist sells a g

When Ford raises pickup truck prices 20 percent and Chevy pickup sales rise 12 percent, in that case these goods are _____ as well as their cross elasticity coefficient is approximately _____. (w) complements; 0.6. (x) substitutes; 0.6. (y) subs

At a $2 price per can, there quantity of applesauce supplied per day is 1000 cases; and at $4, the quantity supplied is 3000 cases per day. Therefore price elasticity of supply is: (i) 2/3. (ii) 1/3.(iii) 3/2. (iv) 1/4. Q : Prevent operating in long run by A monopolist will prevent operating within the long run unless its economic profit is: (i) zero. (ii) positive. (iii) greater than accounting profit. (iv) zero or greater. (v) zero or less. I need a good answer on

A monopolist will prevent operating within the long run unless its economic profit is: (i) zero. (ii) positive. (iii) greater than accounting profit. (iv) zero or greater. (v) zero or less. I need a good answer on

The demand for durable consumer good tends to rise if: (1) Supply rises. (2) Aggregate expenses rise. (3) Consumers predict price hikes or scarcities in the future. (3) Consumers predict surpluses in future. Choose the precise answ

What is Interest rate risk premium? Briefly explain it.

A short run market supply curve for a good manufactured within a purely competitive industry is derived through: (w) vertically summing the marginal cost curves above the AVC curves for all firms which may potentially enter the industry. (x) adding to

Whenever the marginal utility of a good becomes negative or zero: (i) Goods are transformed to the bads. (ii) Net utility reaches the maximum and then declines. (iii) The maximum total advantages have been squeezed from good. (iv) People are unwilling

When the rate of return on investment equals the interest rate, in that case investment will: (w) rise. (x) fall. (y) not change. (z) Any of the above is possible. Hey friends please give your opin

At point a, in below figure the supply curve into this graph: (w) perfectly elastic. (x) relatively elastic. (y) unitarily elastic. (z) relatively inelastic. Discover Q & A Leading Solution Library Avail More Than 1418715 Solved problems, classrooms assignments, textbook's solutions, for quick Downloads No hassle, Instant Access Start Discovering 18,76,764 1932735 Asked 3,689 Active Tutors 1418715 Questions Answered Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!! Submit Assignment

18,76,764

1932735 Asked

3,689

Active Tutors

1418715

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!