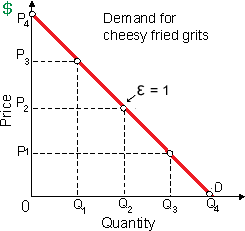

Moving beside the demand curve by Q=0, P4 to Q4, P=0, then elasticity of demand for Pixie’s cheesy fried grits as: (w) doesn't change. (x) falls, then rises. (y) rises, then falls. (z) falls.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.