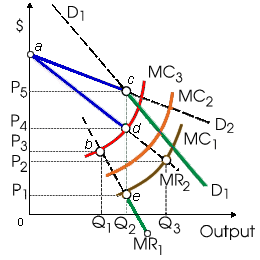

When this firm's marginal cost curve moved upward from MC2 to MC3, the firm would: (w) reduce output from Q3 to Q2 and increase price from P3 to P4. (x) reduce output by Q2 to Q1 and raise price from P4 to P5. (y) not change its price or output. (z) shut down.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?