Total fixed cost in competitive firm

This competitive firm's fixed cost or TFC in demonstrated can be computed as area as: (i) 0P3fq4. (ii) P2P1de. (iii) P3P2ef. (iv) 0P2eq4. (v) aced. Hey friends please give your opinion for the problem of Economics that is given above.

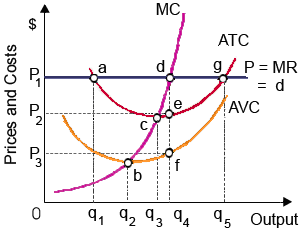

This competitive firm's fixed cost or TFC in demonstrated can be computed as area as: (i) 0P3fq4. (ii) P2P1de. (iii) P3P2ef. (iv) 0P2eq4. (v) aced.

Hey friends please give your opinion for the problem of Economics that is given above.

By 2000, the differential among the rich and the poor which can be attributed to economic discrimination was computed at: (w) approximately 60 percent. (x) approximately 30 percent. (y) under 10 percent. (z) zero.

A purely competitive firm will produce where is: (w) MC is rising. (x) MC = P. (y) MC = MR. (z) All of the above. Can anybody suggest me the proper explanation for given problem regarding Economics

The advantages from the division of labor are improved as workers: (1) Are protected by the barriers which limit the international trade. (2) Who each recognize all facets of production gain an enhanced understanding of the whole project. (3) Constant

Can someone please help me in finding out the accurate answer from the following question. The elasticity of demand for the labor tends to rise as there are increases in the: (i) Amount of capital utilized in a production procedure. (ii) Rate of automation in industry

For an individual price-taker firm, marginal revenue is: (w) another term for profit. (x) constant and equal to price. (y) less than price. (z) negatively sloped. I need a good answer on the topic

At the point of unit elasticity beside the demand curve then a firm faces: (w) profits are always maximized. (x) total revenue is certainly at a maximum. (y) total costs are minimized. (z) All of the above. I need

Possible utilization of a ‘felicific calculation’ to recognize punishments for the crimes was derived from: (1) Medieval scholasticism. (2) Say’s Law. (3) Gresham’s Law. (4) Marshall’s Maxim. (5) Jeremy Bentham&r

This binge drinking exercise observes why excessive drinking might be an economic trouble and the possible influences of government policy.

At a $2 price per can, there quantity of applesauce supplied per day is 1000 cases; and at $4, the quantity supplied is 3000 cases per day. Therefore price elasticity of supply is: (i) 2/3. (ii) 1/3.(iii) 3/2. (iv) 1/4. Q : Reliablity with standard economic Which of the given behaviors is least reliable with standard economic suppositions regarding consumer behavior? (i) Gustav cannot decide which of three distinct combinations of goods he favors. (ii) Lynn hates pickled herring; however Chris is willing

Which of the given behaviors is least reliable with standard economic suppositions regarding consumer behavior? (i) Gustav cannot decide which of three distinct combinations of goods he favors. (ii) Lynn hates pickled herring; however Chris is willing

18,76,764

1927165 Asked

3,689

Active Tutors

1431644

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!