Price increment in elasticity

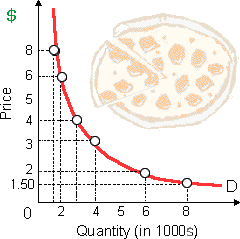

A price hike $4 to $5 per slice of pizza because of total revenue to: (w) fall. (x) remain constant. (y) rise. (z) this is not possible to tell from such data. How can I solve my economics problem? Please suggest me the correct answer.

A price hike $4 to $5 per slice of pizza because of total revenue to: (w) fall. (x) remain constant. (y) rise. (z) this is not possible to tell from such data.

How can I solve my economics problem? Please suggest me the correct answer.

Assume that no externalities in production or consumption exist and the income distribution is universally viewed such as “fair.” When this firm could price discriminate perfectly, one condition for socially optimal output would be for: (i

Can someone please help me in finding out the accurate answer from the following question. The elasticity of demand for the labor tends to rise as there are increases in the: (i) Amount of capital utilized in a production procedure. (ii) Rate of automation in industry

1. Is it possible for any country to have made gains in access (at the expense of quality) of their rural healthcare system, without any gains in efficiency? Explain using a PPF diagram.2. If the own price elasticity for a good is -2.5, what is the l

Technological progress shift: (i) Demand curves up and to right. (ii) Production possibilities curve in the direction of their origins. (iii) Prices into inflationary spiral. (iv) Supply curves rightward from vertical axis. Can som

Can someone help me in finding out the right answer from the given options. Demand curve for the gasoline, a normal good, would shift to right when: (1) The legal least age to drive was raised to 18 all through the world. (2) New oil fields were discovered and exploit

Assume a consumer with the given utility function: U = 3y1y2 + 5. Suppose y2 = 1, derive the marginal utility schedule for y1. In what direction is it moving?

When a monopolist maximizes profit with producing where average total cost is on its minimum, this: (w) should generate an economic profit. (x) should sell at a price equal to marginal cost. (y) will incur an economic loss. (z) will p

Every point beside a vertical demand curve (when there was such a thing) would include a price elasticity coefficient equivalent to: (1) 1. (2) 1. (3) zero. (4) infinity. (5) 1/2. Hey friends please giv

This would be a fallacy to suppose that: (w) a purely competitive firm’s demand curve is perfectly elastic. (x) a purely competitive firm’s supply curve is the marginal cost above the minimum point of the AVC. (y) purely competitive firms generate where MR

By the perspective of society as an entire, in that case land resources are: (w) variable in supply. (x) perfectly elastically supplied. (y) the closest of all resources to generators of pure economic rents. (z) increased through cultivating previousl

18,76,764

1950306 Asked

3,689

Active Tutors

1418694

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!