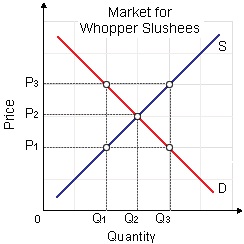

Beginning at equilibrium, a new highest legal price for Whopper Slushees set at P1 would: (i) cause people to purchase more Slushees and fewer cones from Dairy Queen. (ii) Reduce total market demand. (iii) Yield surplus demand and a scarcity. (iv) Increase net market supply. (v) Make surplus supply and a shortage.

Can someone help me in getting through this problem.