Equilibrium price in the short run

The equilibrium price for Christmas trees in the short run is: (w) P1. (x) P2. (y) P3. (z) P4. How can I solve my Economics problem? Please suggest me the correct answer.

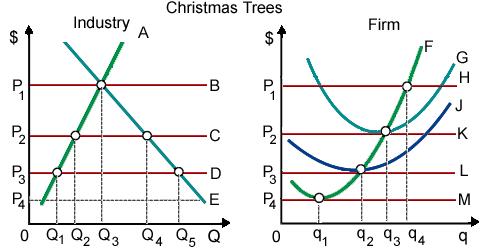

The equilibrium price for Christmas trees in the short run is: (w) P1. (x) P2. (y) P3. (z) P4.

How can I solve my Economics problem? Please suggest me the correct answer.

When Ford raises pickup truck prices 20 percent and Chevy pickup sales rise 12 percent, in that case these goods are _____ as well as their cross elasticity coefficient is approximately _____. (w) complements; 0.6. (x) substitutes; 0.6. (y) subs

Elasticity of Demand: The law of demand elucidates that demand will change due to a change in the price of the commodity. However it does not elucidate the rate at w

An oligopoly is a form of market structure described by: (w) its large number of sellers. (x) firms' capability to easily enter and exit the industry. (y) conscious interdependence. (z) price taker behavior. Q : Minimum Wage Laws I have a problem in I have a problem in economics on Minimum Wage Laws. Please help me in the following question. Minimum wage legislation has been promotes as a technique to: (i) Make sure that workers are paid beneath the subsistence salaries. (ii) Perpetuate poverty. (iii) Maxim

I have a problem in economics on Minimum Wage Laws. Please help me in the following question. Minimum wage legislation has been promotes as a technique to: (i) Make sure that workers are paid beneath the subsistence salaries. (ii) Perpetuate poverty. (iii) Maxim

Increased inequality within the distribution of income into the United States since around 1975 is least attributable to: (1) baby boomers becoming adults. (2) a shift from manufacturing to service industries. (3) the rising percentage of households h

1. Is it possible for any country to have made gains in access (at the expense of quality) of their rural healthcare system, without any gains in efficiency? Explain using a PPF diagram.2. If the own price elasticity for a good is -2.5, what is the l

The dissimilarities in the arc elasticities of demands for labor among the Ajax Corporation and Bosun Limited are consistent along with an inference which Bosun: (1) is a more profitable firm than Ajax. (2) hires more highly skilled workers than Ajax

Separation of ownership or stockholders by control (management) into modern giant corporations tends to divide the economic functions of: (w) capitalists. (x) union leaders. (y) entrepreneurship. (z) bureaucrats. I

When a monopolist maximizes the profit in the product market, it will: (i) Hire labor till the marginal revenue product equivalents the marginal resource cost. (ii) Hire the labor till the value of marginal product equivalents the marginal resource cost. (iii) Pay a w

Normative goals of microeconomics comprise: (w) economic growth. (x) price-level stability. (y) high employment. (z) equity within the distribution of income. Please friends choose one choice from the above. I want your suggestion

18,76,764

1929070 Asked

3,689

Active Tutors

1438869

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!