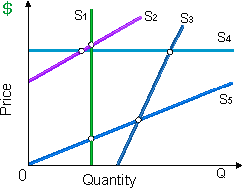

Suppose that all these given demonstrated curves in below are infinitely long straight lines. There supply curve that is perfectly price-inelastic is: (i) supply curve S1. (ii) supply curve S2. (iii) supply curve S3. (iv) supply curve S4. (v) supply curve S5.

How can I solve my Economics problem? Please suggest me the correct answer.