Define progressive in taxes as percentage of income

Line T0 depicts a tax system which is: (1) progressive. (2) recessive. (3) proportional. (4) biased. (5) regressive. Hey friends please give your opinion for the problem of Economic that is given above.

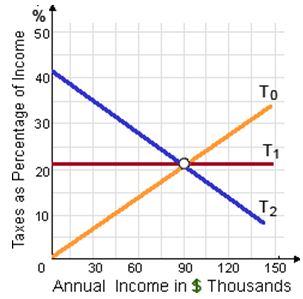

Line T0 depicts a tax system which is: (1) progressive. (2) recessive. (3) proportional. (4) biased. (5) regressive.

Hey friends please give your opinion for the problem of Economic that is given above.

Can someone please help me in finding out the accurate answer from the following question. The most general legal form of business in United States is: (1) Sole proprietorships. (2) Partnerships. (3) Cooperatives. (4) Corporations.

On Indian industry what are the effects of globalization?

A profit-maximizing monopolist will necessarily incur economic losses when, at every feasible level of output as: (w) average fixed costs [AFC] are very high. (x) average total costs [ATC] lies above the demand curve. (y) average tota

Pure competition yields economic efficiency through: (w) punishing profit maximizing behavior. (x) forcing firms to adopt the least costly technologies available. (y) generating high profits as incentives. (z) rewarding entrepreneurs

When the New York City government only permits landlords to charge $800 a month for a little apartment while equilibrium rent would be $1,500, this has imposed: (w) price floor. (x) regulation which will result in market surpluses. (y) regulation that

By the perspective of society as an entire, in that case land resources are: (w) variable in supply. (x) perfectly elastically supplied. (y) the closest of all resources to generators of pure economic rents. (z) increased through cultivating previousl

A purely competitive firm maximizes profit through producing where is: (w) P = ATC. (x) P = MR = MC. (y) PQ = TC. (z) AFC = AVC. I need a good answer on the topic of Economics problems. Please give

I have a problem in economics on fixed input in short run. Please help me in the following question. Which of the given below is most likely to be the fixed input in short run for General Motors? (i) An assembly line worker. (ii) Paint for cars. (iii)

Whenever unions and managers have failed to arrive at a collective bargaining agreement and workers reject to leave the production facility owned by firm, the union’s strategy is termed as: (i) Boycott or an embargo. (ii) Management lock-out. (i

A purely competitive firm has a supply curve which is: (w) perfectly elastic. (x) relatively inelastic. (y) flatter than its demand curve. (z) upward sloping as output increases. Hello guys I want

18,76,764

1960292 Asked

3,689

Active Tutors

1418091

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!