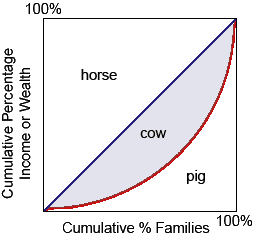

The areas illustrates in this Lorenz diagram can be used to compute a Gini index as: (i) (cow + pig)/cow. (ii) cow2/(cow + pig). (iii) pig2/(cow + pig). (iv) cow/(cow + pig) (v) (cow + horse)/pig.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?