Calculate of total variable in an area

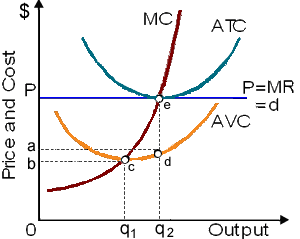

Total variable costs can be estimate as: (1) 0bcq1. (2) 0adq2. (3) 0Peq2. (4) aPed. (5) Cannot be measured within demonstrated figure. Hey friends please give your opinion for the problem of Economics that is given above.

Total variable costs can be estimate as: (1) 0bcq1. (2) 0adq2. (3) 0Peq2. (4) aPed. (5) Cannot be measured within demonstrated figure.

Hey friends please give your opinion for the problem of Economics that is given above.

The resource least probable to conform to the supply curve demonstrated in this figure would be: (w) land. (x) capital. (y) labor. (z) entrepreneurship. Q : Define forward shifting of tax burden The greater the price elasticity of demand associate to the price elasticity of supply, then the: (i) greater the legal incidence of any tax burden. (ii) smaller the forward shifting of any tax burden. (iii) smaller the backward shift

The greater the price elasticity of demand associate to the price elasticity of supply, then the: (i) greater the legal incidence of any tax burden. (ii) smaller the forward shifting of any tax burden. (iii) smaller the backward shift

Policies which raise the overall demand for labor and maintain unemployment rates low are: (w) significant for the success of any other programs to reduce poverty. (x) sufficient measures to reduce the incidence of poverty. (y) not relevant to the suc

In which market condition, the effect of an individual seller is (0) zero? Answer: In Perfectly Competitive market condition.

The strategy which is most likely to yield the maximum wages and employment and the most economic clout for all the workers over long run would be for a union to: (i) Restrict entry to a specific occupation. (ii) Boycott non-unionized firms which compete with the unio

I have difficulty in this question. Provide me correct solution of this economy question. Compare & contrast the supposition of monopolistic competition along with perfect competition & monopoly.

The problem of asymmetric information is that

When one firm controls all production and the price of a good without shut substitutes, there is: (i) monopoly market structure. (ii) violation of the law of demand and supply. (iii) lack of equity although assurance of efficiency. (iv) legal barrier to entry. (v) cer

In the market economies, resources are finally owned by the: (i) Corporations which dominate the economic activity. (ii) Proprietorships and partnerships. (iii) Business firms collectively. (iv) Individual house-holds. (v) Government acting as the social trustee.

Assume that a main oil spill occurred off the Alaskan coast within the waters where many wild salmon Americans eat is caught. So, what will occur to the price and supply of salmon within the US? (w) no change (x) supply = fall, price = rise

18,76,764

1939851 Asked

3,689

Active Tutors

1434736

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!