Least probable resource for supply curve

The resource least probable to conform to the supply curve demonstrated in this figure would be: (w) land. (x) capital. (y) labor. (z) entrepreneurship. Can anybody suggest me the proper explanation for given problem regarding Economics generally?

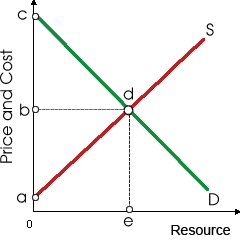

The resource least probable to conform to the supply curve demonstrated in this figure would be: (w) land. (x) capital. (y) labor. (z) entrepreneurship.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?

For the purely-competitive cranberry market, as in below figure there Curve H is: (i) industry’s long-run supply curve. (ii) firm’s demand curve in the short run. (iii) industry’s marginal cost curve. (iv) firm’s long run margi

If marginal social cost (MSC) equivalents marginal social benefit (MSB) as: (i) no injurious pollutants are being pumped within the environment. (ii) consumers enjoy more surplus than do producers. (iii) producers surplus is minimized

The following is a case problem around which the examination paper will be based. In preparation for the examination, you should study the problem scenario and identify the possible public international law issues which might arise, and how the law might be applied to

When the equality standard of income distribution were adopted: (w) people would be paid the values of their marginal products. (x) family incomes would be identical for families of all sizes. (y) poets and engineers would have the same incomes. (z) g

The Purely competitive labor markets are not characterized through: (1) Most of the individual sellers and buyers of labor services. (2) Wages equivalent to the marginal resource costs. (3) Labor unions. (4) Price taking sellers and buyers of the labo

Within the long run, a monopoly cannot continually produce economic profit unless: (w) economies of scale are important. (x) corporate taxes are lowered. (y) barriers to entry are significant. (z) the monopolist maximizes profit.

Graduate Level Problem Set. First question is in relation to the article the Population Problem: Theory and Evidence by Partha Dasgupta.

The competitive firm will demand more labor when: (i) Technological advances support automation. (ii) The price of firm's output increases. (iii) More firms enter in the industry. (iv) The value of marginal product is beneath the wage rate. (v) Worker

Profit maximization needs a purely competitive firm to manufacture at an output level where: (i) marginal revenue > marginal cost. (ii) marginal cost equals the competitive price. (iii) marginal cost is falling. (iv) marginal reven

Provide solution of this question. Supposing no other changes, if balances in small time deposits increase by $30 billion and money market mutual funds held by businesses decrease by $30 billion, the: A) M1 and M2 money supplies will not change. B) M2 and MZM money su

18,76,764

1941578 Asked

3,689

Active Tutors

1425372

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!