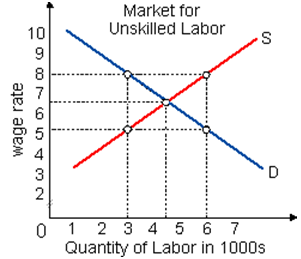

Boosting minimum wage laws from $5 to $8 per hour is LEAST probable to: (w) give some unskilled workers with higher incomes. (x) cause some low-wage workers to lose their jobs. (y) raise friendship like a basis for employment. (z) decrease unemployment between unskilled workers.

Hey friends please give your opinion for the problem of Economic that is given above.