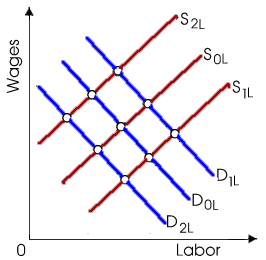

When this purely competitive labor market is primarily in equilibrium at D0L, S0L, a moving step to equilibrium at D1L, S0L would be probably to follow from increases in: (w) imports of this good by foreign competitors. (x) workers’ demands for greater leisure. (y) skill levels required to operate newly adopted technologies. (z) the price of output.

Please choose the right answer from above...I want your suggestion for the same.