Price elasticity of demand DVDs of games

Moving from point c to point d beside demand curve D, the price elasticity of demand DVDs of video games equals: (1) 0.8. (2) one. (3) 1.10. (4) 1.25. (5) 2.50 Can someone explain/help me with best solution about problem of Economics...

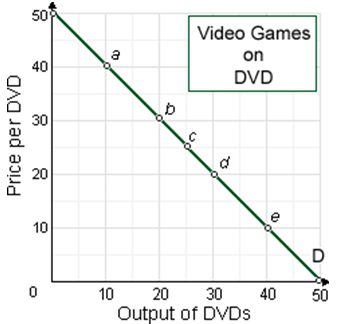

Moving from point c to point d beside demand curve D, the price elasticity of demand DVDs of video games equals: (1) 0.8. (2) one. (3) 1.10. (4) 1.25. (5) 2.50

Can someone explain/help me with best solution about problem of Economics...

An individual or organization which simultaneously purchases low and sells high in various markets is a/an: (i) Angel duster. (ii) Escalator. (iii) Arbitrageur. (iv) Finagler. (v) Optimizer. Can someone please help me in find

When the real wage increases, an extra unit of: (1) Labor supplied will purchase fewer goods. (2) Leisure is more costly. (3) Output needs more labor time. (4) Capital becomes more highly employed. Find out the right answer from th

When the price elasticity of demand for goose grease is 2.5 and a 10% price hike will reasons of quantity demanded to: (w) grow by roughly 2.5%. (x) grow by roughly 25%. (y) fall by roughly 25%. (z) fall by roughly 4%. Q : Buying low price-riskless selling at Buying low within one market and riskless selling at a higher price into another is termed as: (1) speculation. (2) arbitrage. (3) capitalization. (4) marketeering. (5) profiteering. Please choose the right answer from above...I wa

Buying low within one market and riskless selling at a higher price into another is termed as: (1) speculation. (2) arbitrage. (3) capitalization. (4) marketeering. (5) profiteering. Please choose the right answer from above...I wa

Severe drought outcomes in a drastic fall in the output of wheat. Examine how will it influence the market price of wheat? Answer: As an outcome of severe drought,

Can someone please help me in determining the right answer from the following question. The three fundamental assumptions required to construct a model of the production possibilities frontier do not comprise: (1) Reducing marginal returns to producti

For Christmas tree in this market, Curve H is this: (w) industry’s long-run supply curve. (x) firm’s demand curve in the short run. (y) industry’s marginal cost curve. (z) firm’s long run marginal cost curve.

The short-run shutdown price arises where price: (w) equals AFC at the minimum. (x) is below ATC and above AVC. (y) equals AVC at its minimum point. (z) is above MR. Hey friends please give your opinion for the pro

The percentage change within quantity demanded along this demonstrated linear demand curve is: (w) greater than the percentage change within price in range b. (x) smaller than the percentage change within price in range a. (y) precise

Question: Describe the differences between shifts in demand and movements along the demand curve. What are the main factors which can shift the demand curve? Explain why they cause the demand curve to shift. Use e

18,76,764

1956655 Asked

3,689

Active Tutors

1434555

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!