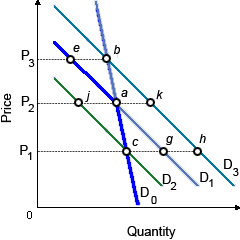

In this illustrated figure kinked demand curve model, there two demand curves intersect at point a since the other oligopolistic firms: (w) are rapid to follow both price increases and price decreases by rival firms. (x) will follow price decreases but that are unlikely to follow a competitor’s price increase. (y) can’t decide whether the demand curve they face is D1 or D2. (z) face volatile and ever changing demands for their products.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.