Most perfectly price inelasticity in supply curve

In illustrated graph below, supply is mostly perfectly price inelastic at: (i) point a. (ii) point b. (iii) point c. (iv) point d. Hey friends please give your opinion for the problem of Economics that is given above.

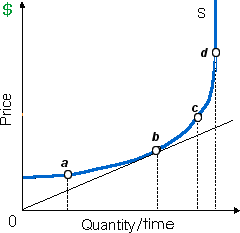

In illustrated graph below, supply is mostly perfectly price inelastic at: (i) point a. (ii) point b. (iii) point c. (iv) point d.

Hey friends please give your opinion for the problem of Economics that is given above.

Short-run market supply curve of a competitive industry is derived by summing all the firms’: (1) average cost curves vertically. (2) short-run supply curves horizontally. (3) production capacities along with the resources available. (4) individ

Transfer payments and progressive tax policies are being determinate to: (w) reduce disparities in the distributions of income and wealth. (x) shift the Lorenz curve toward a position of less income equality. (y) have no net effect on income equality

The demand for an exact good tends to be relatively more price elastic when the good: (1) has various close substitutes and very little complements. (2) is taken as a necessity in place of a luxury. (3) is an inferior good. (4) is rel

Can someone help me in finding out the right answer from the given options. The supply curve reveals the highest: (i) Stock on hand in inventory. (ii) Gains a firm makes by selling varying quantity of a good. (iii) Quantity of a good which sellers will offer at differ

The extent of equality within the income distribution of a country seems to depend most heavily upon the degree of: (w) economic development in the country. (x) progress towards national socialism. (y) central economic planning. (z) fertility of the a

In this demonstrated figure, there the price elasticity of demand coefficient is: (1) one at the midpoint. (2) greater than one in range a. (3) less than one in range b. (4) falling along with movements down along the demand curve. (5) All of the abov

The supply curve for perishable goods which, once produced, can’t be stored in inventory is generally functioned as perfectly price inelastic into the: (i) short-run. (ii) intermediate period. (iii) long-run. (iv) market period. (v) fiscal year

If, throughout a period while video iPods are gaining popularity, the technology to create them enhances, in that case demand: (w) and supply would both decrease. (x) and supply would both increase. (y) increases when supply decreases. (z) decreases when supply

When a purely competitive industry is into long run equilibrium, in that case a typical firm can: (w) earn normal accounting profit although only zero economic profit. (x) incur economic losses when these are offset by accounting prof

Assume that a student takes out a college loan which needs 12% annual interest, however later learns that his aunt makes loans to the family members at 5% interest. The student has suffered from the problem termed as: (1) Rational ignorance. (2) Blind indifference. (3

18,76,764

1930560 Asked

3,689

Active Tutors

1423424

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!