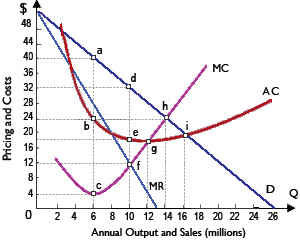

Prohibition Corporation could attain minimum average costs for its St. Valentine’s Day software when this produced: (1) 4 million copies. (2) 6 million copies. (3) 8 million copies. (4) 10 million copies. (5) 12 million copies.

Can anybody suggest me the proper explanation for given problem regarding Economics generally?