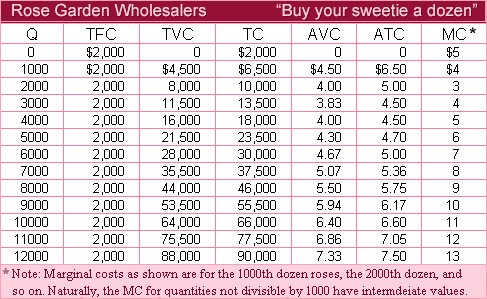

When the wholesale price P = $4 per dozen roses, it purely competitive increased farm maximizes profit through producing ___ dozen roses at a total (profit /loss) of $___. (1) zero; loss; $2000. (2) 2000; loss; $1500. (3) 3000;profit; $1500. (4) 4000; profit; $4,500. (5) 4000; profit; $2,000.

How can I solve my Economics problem? Please suggest me the correct answer.