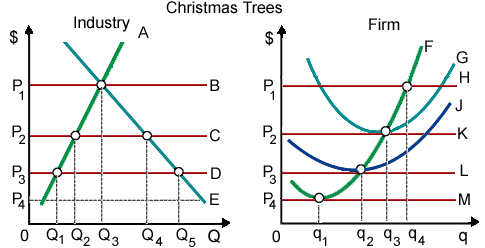

When this firm is typical in this purely competitive market, in that case long-run equilibrium for Christmas trees will be reached at a market price is of: (1) P1. (2) P2. (3) P3. (4) P4. (5) Not computable from these figures.

Please choose the right answer from above...I want your suggestion for the same.