Market-period supply curve

For a purely competitive industry a market-period supply curve would be: (i) curve A. (ii) curve B. (iii) curve C. (iv) curve D. (v) curve E. Hello guys I want your advice. Please recommend some views for above Economics problems.

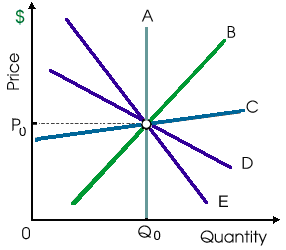

For a purely competitive industry a market-period supply curve would be: (i) curve A. (ii) curve B. (iii) curve C. (iv) curve D. (v) curve E.

Hello guys I want your advice. Please recommend some views for above Economics problems.

When a monopolist which does not price discriminate maximizes profit and charges a price equal to marginal cost, this will: (i) minimize average cost and generate zero economic profit. (ii) minimize average cost and generate a positiv

Nintendo Co. of Japan has been accused of discarding its products (as selling below cost) upon the U.S. market that harms U.S. producers. When true, it is an illustration of: (w) excessive international competition. (x) protectionism. (y) aggressive advertising. (z) p

Normal 0

Surveys or Polls: The word survey or poll usually describes a method of gathering information from a sample of individuals. In contrast to a census, where all members of the population are studied, surveys collect details from only a part of a populat

When a price hike from $15 to $20 for DVD disks causes sales of DVD players to reduce from 100 to 50 units, in that case the coefficient of cross-elasticity of demand among these goods is approximately: (w) 1/10. (x) 10. (y) 7/3. (z)

Definition of law of demand: It is the claim that, other things equivalent, the quantity demanded of a good drops/falls whenever the price of the good increases.

Average cost: It is the cost per unit of output.

The worker who signed a yellow dog contract in the year 1920s agreed: (i) To support the union’s feather-bedding efforts. (ii) Not to work with the ‘scab’ non-union strike-breakers. (iii) To pay the union dues as protection from the violent union org

The income elasticity of demand is a measure of the: (w) relative responsiveness of quantity demanded to changes within income. (x) absolute change within demand yielded by an absolute change within income. (y) slope of the income-consumption curve. (

The income stream per period like a percentage of the dollar outlay for investment into a capital good is the: (1) present value of the investment good. (2) rate of economic profit. (3) interest rate. (4) rate of retu

18,76,764

1925679 Asked

3,689

Active Tutors

1446655

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!