Goods and services

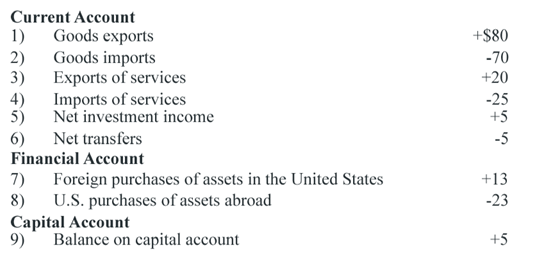

Refer to the above data. Choose the right answer from following. Zabella's balance on goods and services illustrates a: A) $5 billion deficit. B) $5 billion surplus. C) $10 billion surplus. D) $15 billion deficit.

When a decreasing cost industry is purely competitive in that case: (1) each firm’s long-run supply curve is downward sloping. (2) each firm encounters increasing returns to scale. (3) growth of industry output yields lower per unit costs. (4) c

I have a problem in economics on Supply of Labor: Income and Substitution Effects. Please help me in the following question. When the income effect of higher wage rate is more influential than the substitution effect, then: (1) The supply curve of labor is positively

Give the answer of following question. Negative externalities arise: A) when firms pay more than the opportunity cost of resources. B) when the demand curve for a product is located too far to the left. C) when firms "use" resources without being compelled to pay for

Within this "kinked-demand curve" model, that firm views the demand curve this faces as the: (w) linear "kinked" demand curve aD2 for all prices. (x) linear "kinked" demand curve D1D1 for all prices. (y) nonlinear "kin

The profit-maximizing firm which is perfectly competitive in the resource market however which consists of market power in the output market will hire the labor at a point where: (p) VMP = MRP = MFC = w. (q) VMP > MRP = MFC = w. (r) VMP = MRP = MFC > w. (s) VMP

If all US Treasury bonds are perpetuities that annually pay the sum of one thousand and 00/100 dollars [$1000] each year, always, to the holder of this bond starting one year from today and if the current market price of such bond wer

Preceding to the merger of the American Federation of Labor and Congress of Industrial Organizations to the AFL CIO merger in year 1955: (1) The AFL was an alliance of the industrial unions. (2) The CIO was an alliance of the craft unions. (3) Jurisdictional strikes o

I have a problem in economics on Problem on Industrial Unions. Please help me in the following question. The United Auto Workers (or UAW) is an illustration of a(n): (1) Mechanical union. (2) Company union. (3) Craft union. (4) Industrial union.

All markets which are really relevant for human beings are exemplified by: (1) Extensive advertising, sales promotions and marketing. (2) Demands from each and every individual for all products. (3) Potential buyers willing to reimburse and potential

I have a problem in economics on Short Run-input of firms cannot be changed. Please help me in the following question. In short run, the firm: (i) Can change any input. (ii) Can’t change any input. (iii) Cannot change the output. (iv) Has at lea

18,76,764

1949940 Asked

3,689

Active Tutors

1446502

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!