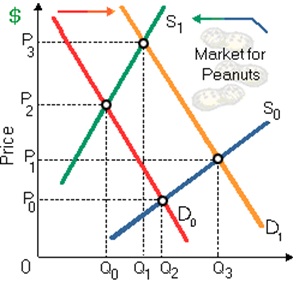

As per such supply and demand curves for peanuts, there is the: (w) demand for peanuts has fallen. (x) price rises to P1 due to better peanut technology. (y) production of peanuts was initially Q0. (z) new equilibrium price of peanuts is P3.

Please choose the right answer from above...I want your suggestion for the same.