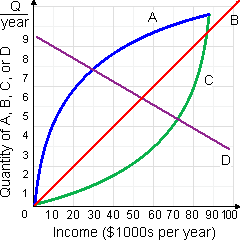

This below figure demonstrates how consumption of goods A, B, C and D changes as a family’s income changes. When income increases, the income elasticity of demand is positive although declining for: (w) good A. (x) good B (y) good C. (z) good D.

How can I solve my economics problem? Please suggest me the correct answer.