Consumption curve

Illustrate a point on consumption curve at which APC = 1. Answer: APC = C/Y = 1 is possible when C = Y, that is, Consumption is equivalent to Income.

Illustrate a point on consumption curve at which APC = 1.

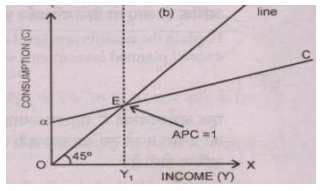

Answer:

APC = C/Y = 1 is possible when C = Y, that is, Consumption is equivalent to Income.

Can someone help me in finding out the right answer from the given options. The basic difference between the dollar amounts people would willingly to pay for a particular quantity of a good and the amounts that they do pay at a particular market price is termed as: (1

Analyze at least 3 possible regions for the industry which could lead to transaction costs, explaining each in detail.

Illustrate whether output generated for self consumption is comprised or not comprised in the value of output? Answer: The output generated for self consumption is

A family’s newly constructed home can produce the service of shelter across several years, therefore from a macroeconomic perspective, this is most reasonably classified as: (i) economic capital. (ii) social infrastructure. (iii) market capitalization. (iv) a fi

Describe Okun's law? Give an illustration of how it works.

The Income effects will be most strongly positive for: (1) Normal goods. (2) Necessities. (3) Superior or luxury goods. (4) Substitutes and much negative for the complements. Find out the right answer from the above options.

Illustrate which budget expenses does not result in the creation of assets or reduction of liability. Give illustrations too.

Examples of command economies are: a) the United States and Japan b) Sweden and Norway c) Mexico and Brazil d) Cuba and North Korea

Multiplier: The Multiplier is the ratio of change in income by the change in investment. Multiplier (k) = ΔY/ΔI

Question: Was the stimulus package passed in 2009 as success? In answering this question the focus should be the articles on the syllabus, but you should also include opinions of other commentators. &nbs

18,76,764

1958514 Asked

3,689

Active Tutors

1457418

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!