Where is demand perfectly price inelastic at price

For Pixie's cheesy fried grits demand is perfectly price inelastic at a price of: (w) P4. (x) P2. (y) 0. (z) None of the above. Please choose the right answer from above...I want your suggestion for the same.

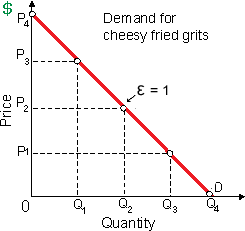

For Pixie's cheesy fried grits demand is perfectly price inelastic at a price of: (w) P4. (x) P2. (y) 0. (z) None of the above.

Please choose the right answer from above...I want your suggestion for the same.

Choose the right answer of the following problem. "The government deregulated the electricity industry in California and a shortage of electricity occurred soon . It is clear that the deregulation caused the shortage." This statement requires careful analysis becau

When the market price is beneath the equilibrium price then: (i) The market will clear. (ii) An excess exists. (iii) Consumers will not invest. (iv) The shortage exists. (v) Each and every consumer will be satisfied. Find out the r

Harvey is currently a Junior Analyst at a financial firm. His annual salary is $30,000, and past experience leads him to believe that the real (inflation adjusted) value of his salary will remain at that level in the future. (Assume he is paid at the end o

Sally is very rich that money hardly matters to her, although when the price of JIF chunky peanut butter doubled Sally switched to Peter Pan chunky peanut butter. This alters is an example of the: (1) Income effect. (2) Payback effect. (3) Substitution effect. (4) Pri

Explain the term PHP?

I have a problem in economics on Marginal factor Costs. Please help me in the given question. The synonymous words marginal factor costs or marginal resource costs signify to the: (p) Cost incurred in generating an additional unit of the capital. (q) Cost to the resou

Illustrations of goods which are close substitutes comprise: (i) Technology and capital. (ii) Motorcycles and helmets. (iii) Chopsticks and forks. (iv) Cowhides and beef. Find out the right answer from the above op

The minimum revenue which will induce a firm to produce a specified output in place of shutting down into the short run is the: (a) maximum such consumers are willing to pay for that output. (b) total variable cost of producing such output. (c) short-

When diet faddists gulp 205 million unsweetened as “No-Carb” milkshakes of $2.30 apiece, if cut back to 155 million per week while the price rises to $3.70 every, the price elasticity of their demand for shakes equivalents

In equilibrium for the firm with power to adjust the salary it pays, then the rate of monopsonistic exploitation equivalents any difference among: (i) VMP and MFC. (ii) MRP and MFC. (iii) P and MC. (iv) MRP and w. (v) MR and w. Fin

18,76,764

1942007 Asked

3,689

Active Tutors

1461195

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!