Variation in price elasticity as price of output

The only supply curve which has price elasticity which varies as the price of output increases is within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D. Hello guys I want your advice. Please recommend some views for above Economics problems.

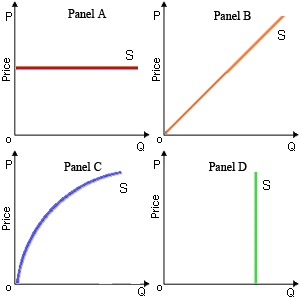

The only supply curve which has price elasticity which varies as the price of output increases is within: (w) Panel A. (x) Panel B. (y) Panel C. (z) Panel D.

Hello guys I want your advice. Please recommend some views for above Economics problems.

When will a rise in demand entail an increase in the quantity demanded however no change in the price?

When the price of hot dogs rises, you would suppose the demand for: (i) mustard to rise. (ii) Hot dogs to reduce. (iii) Buns to rise. (iv) Hot dogs to rise. (v) Buns to reduce. Find out the right answer from the above options.

An accusation of predatory pricing is complicated to prove within a court of law since: (w) firms generally have too much power. (x) consumers and juries like the low prices and are less likely to fine a firm for lowering price. (y) predatory behavior

Can someone help me in finding out the right answer from the given options. The Moral hazards which produce shirking by employees can be partly remedied when firms adopt the policies of: (1) Efficiency salaries. (2) Hierarchical signaling. (3) Careful screening throug

Bobby Lee’s dairy has gainfully expanded beyond butter, fresh milk and cheese, by providing Organizmic Fertilizer, guided by ATV tours for the visitors, and Granny Lee’s Exfoliating Body Yogurt. The Clyde County Business News trumpets that the Bobby Lee ha

I have a problem in economics on Basic definition of Production. Please help me in the following question. Production is the process in which: (i) Technology and human knowledge are utilized to apply energy to convert materials to make them more preci

When there is an excess in the balance of trade? Answer: When export > import (that is, when export is greater than import).

I have a problem in economics on short run demand. Please help me in the following question. In short run, the demand mainly depends most on: (1) Supply. (2) Costs of production. (3) Consumer tastes and preferences. (4) Technology. (5) Resource access

The maximum amounts of a good that people are willing and capable to buy at different market prices during a specific period are depicted by: (1) Horizontal summations. (2) Income or satisfaction boundaries. (3) Demand curves. (4) Consumption possibilities frontiers.<

When the price of a financial asset is $1,000 and the interest rate is 10 percent, in that case investment is not justified for: (1) a perpetuity paying $100 annually. (2) an income stream paying $500, $400, and $300, respectively, at the ends of all

18,76,764

1929443 Asked

3,689

Active Tutors

1417350

Questions Answered

Start Excelling in your courses, Ask an Expert and get answers for your homework and assignments!!