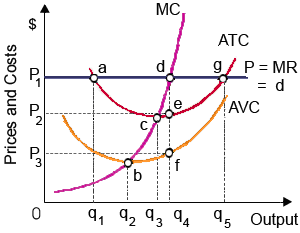

Total revenue (i.e., TR=PQ) for such profit-maximizing competitive firm equals area as: (a) 0P1gq5. (b) 0P1dq4. (c) 0P2cq3. (d) P2P1de. (e) 0P2eq4.

I need a good answer on the topic of Economics problems. Please give me your suggestion for the same by using above options.